At Osa Property Management, we understand that owning rental properties can significantly impact your tax situation. Many landlords wonder, “How does a rental property affect your taxes?”

This blog post will explore the key tax implications of rental property ownership, including income reporting, deductible expenses, and the consequences of selling your investment. We’ll provide practical insights to help you navigate the complex world of rental property taxation and maximize your financial benefits.

What Counts as Rental Income?

The Basics of Rental Income

Rental income includes more than just monthly rent checks. The IRS considers various payments as taxable rental income. Property owners must understand these different types to ensure accurate tax reporting.

Monthly Rent and Beyond

Monthly rent payments form the core of rental income. However, other payments also fall under this category:

- Advance Rent: Report this income in the year you receive it, even if it covers future periods. For example, if a tenant pays January 2026 rent in December 2025, include it on your 2025 tax return.

- Security Deposits: Generally, these don’t count as income when received if you plan to return them. However, any portion you keep due to damage or lease violations becomes taxable income in the year you retain it.

Less Obvious Income Sources

Some rental income sources might surprise property owners:

- Lease Cancellation Payments: If a tenant pays to break their lease early, this counts as rental income.

- Tenant-Paid Expenses: All rental income must be reported on your tax return, and in general the associated expenses can be deducted from your rental income.

- Non-Cash Payments: The fair market value of property or services received instead of money (e.g., a tenant painting the unit in exchange for rent) counts as taxable income.

Reporting Rental Income on Tax Returns

Most rental property owners use Schedule E (Form 1040) to report income and expenses. This form allows listing of multiple properties and provides sections for various expense types.

Property management services (like those offered by Osa Property Management) often provide detailed income statements, which simplify the process of completing Schedule E. These records clearly differentiate between income types, ensuring accurate reporting.

Even if expenses exceed rental income for the year, resulting in a loss, you must report all income received. The IRS scrutinizes rental activities closely, so accurate reporting helps avoid audits or penalties.

Special Considerations

In some cases, rental activities might be considered a business rather than passive income. This typically applies when substantial services (like regular cleaning or meal services) are provided to tenants. In such situations, income and expenses are reported on Schedule C instead of Schedule E.

As we move forward, let’s explore the flip side of rental income: the expenses you can deduct to offset your tax liability.

What Expenses Can You Deduct for Rental Properties?

Common Deductible Expenses

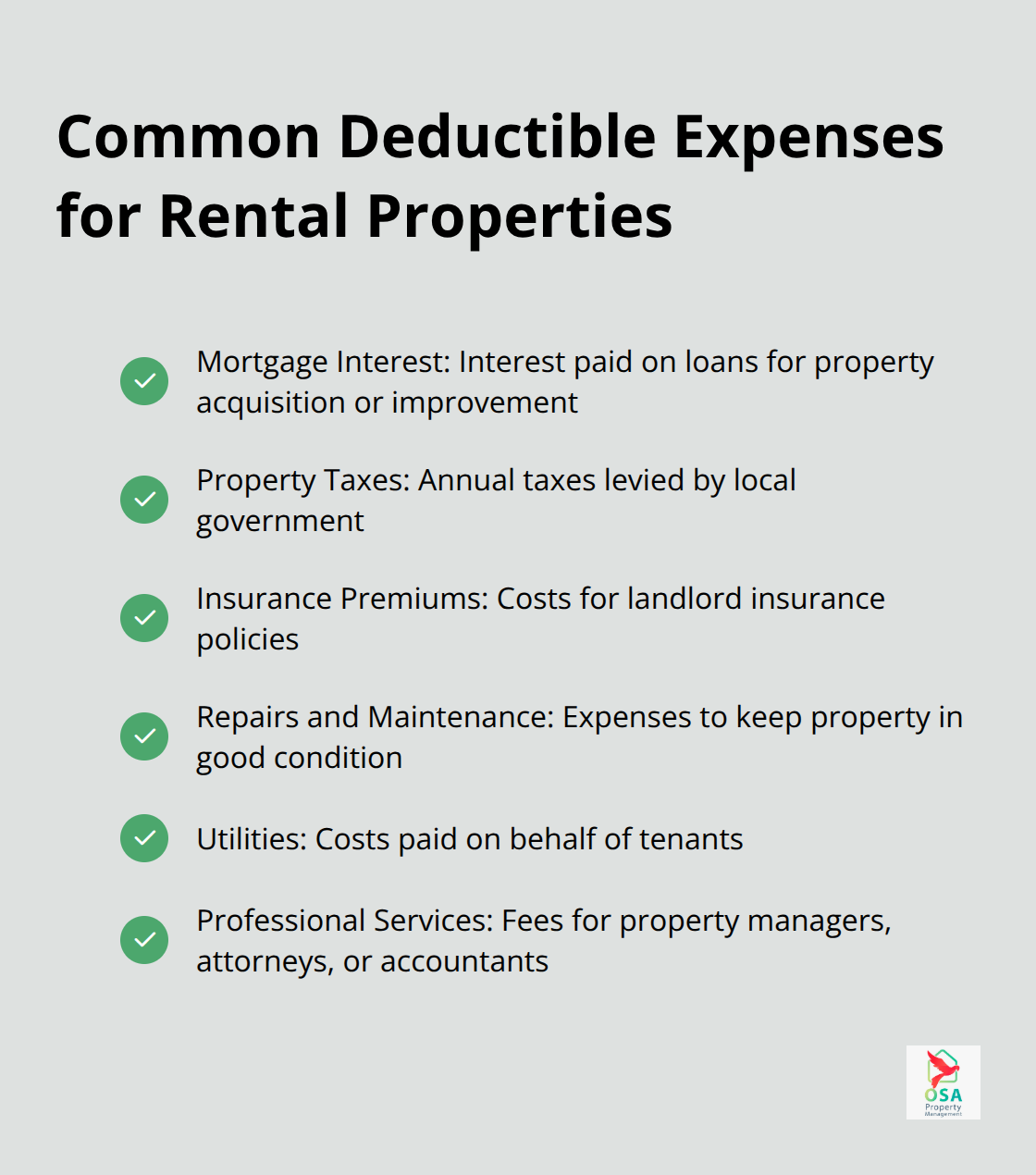

The IRS allows landlords to deduct various expenses related to their rental properties. These deductions can significantly reduce your tax liability. Here are some of the most common deductible expenses:

- Mortgage Interest: You can deduct the interest paid on loans used to acquire or improve your rental property (often one of the largest deductions).

- Property Taxes: Annual property taxes levied by your local government qualify for full deduction.

- Insurance Premiums: Premiums for landlord insurance policies (including liability and property damage coverage) count as deductible expenses.

- Repairs and Maintenance: Costs to keep your property in good condition (e.g., fixing leaky faucets or repainting) are deductible in the year you incur them.

- Utilities: Any utilities you pay on behalf of your tenants become deductible costs.

- Professional Services: Fees paid to property managers, attorneys, or accountants for rental property-related services qualify for deduction.

Understanding Depreciation

Depreciation offers a powerful tax benefit for rental property owners. Under the General Depreciation System (GDS), residential rental property is depreciated over 27.5 years.

To calculate your annual depreciation deduction:

- Determine your property’s basis (usually the purchase price plus certain closing costs and improvements).

- Subtract the value of the land (land doesn’t depreciate).

- Divide the remaining amount by 27.5.

For example, if you purchased a rental property for $300,000 and the land is valued at $50,000, your depreciable basis would be $250,000. Your annual depreciation deduction would be approximately $9,090 ($250,000 ÷ 27.5).

Record-Keeping Requirements

Accurate record-keeping proves essential for claiming rental property deductions. The IRS requires you to keep records that support your reported income and deductions. Maintain the following:

- Purchase documents for your property

- Receipts for all property-related expenses

- Bank statements showing rental income deposits

- Copies of lease agreements

- Records of any improvements made to the property

Special Considerations

Some expenses might seem deductible but actually require special treatment:

- Capital Improvements: Major upgrades that add value to the property (e.g., a new roof) must be depreciated over time rather than deducted in full in the year of the expense. In 2024, the bonus depreciation deduction under section 168(k) will be reduced from 80% to 60%.

- Personal Use: If you use the property personally for part of the year, you must prorate your expenses between rental and personal use.

- Start-up Costs: Expenses incurred before you begin renting the property might need to be capitalized and deducted over time.

Understanding these deductions can help you maximize your rental property’s profitability. However, tax laws can be complex and change frequently. To ensure you follow all IRS guidelines and maximize your benefits within the law, consider consulting with a tax professional or a reputable property management company (such as Osa Property Management for properties in Costa Rica).

Now that we’ve covered deductible expenses, let’s explore what happens when you decide to sell your rental property and the tax implications that come with it.

What Happens When You Sell Your Rental Property?

Capital Gains Tax Implications

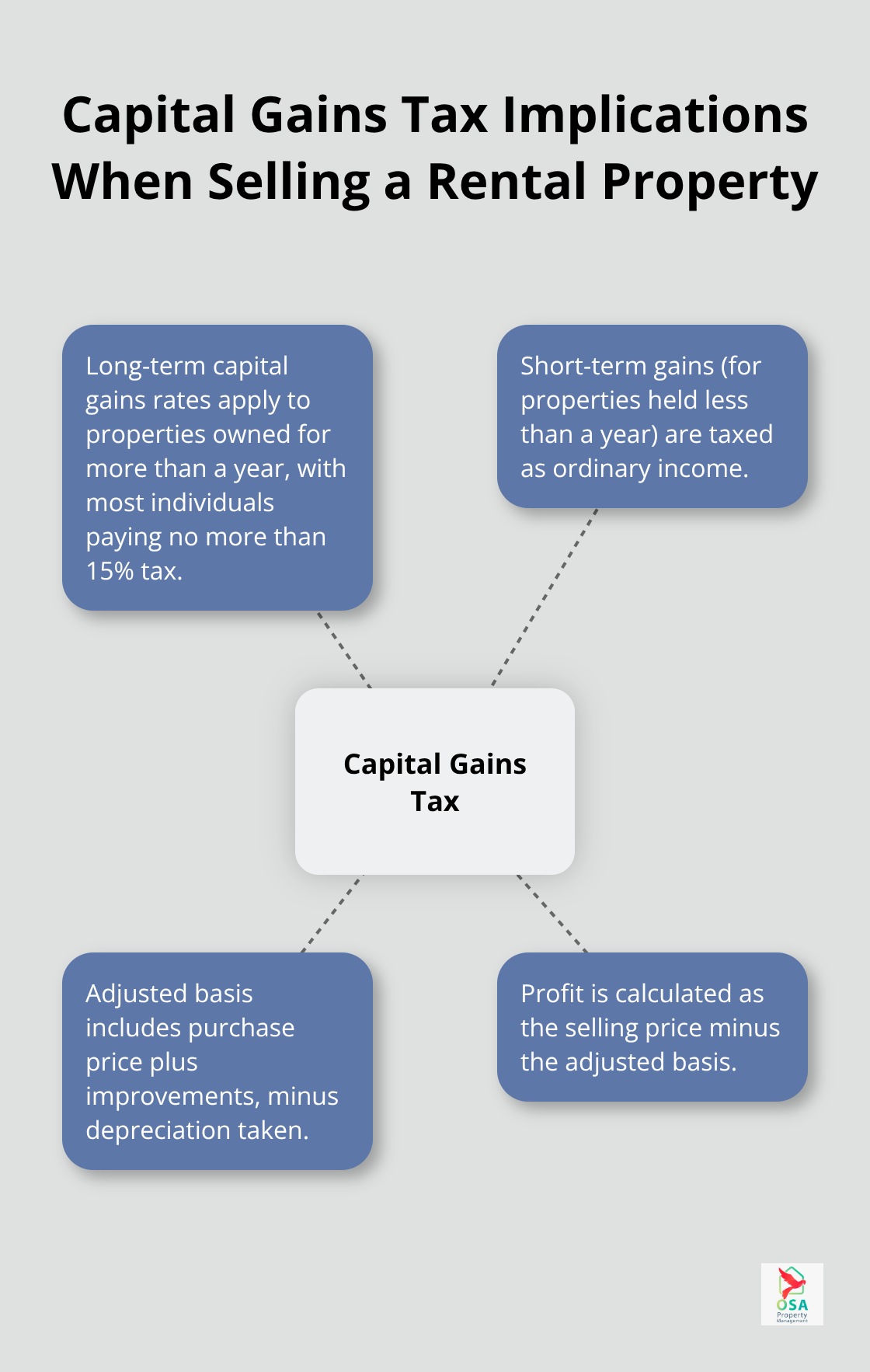

When you sell a rental property for more than your adjusted basis, you must pay capital gains tax on the profit. The adjusted basis typically includes your purchase price plus improvements, minus depreciation taken.

Long-term capital gains rates apply to properties owned for more than a year. As of 2024, the tax rate on most net capital gain is no higher than 15% for most individuals. Short-term gains (for properties held less than a year) are taxed as ordinary income.

For example, if you bought a property for $200,000, made $50,000 in improvements, took $30,000 in depreciation, and sold it for $300,000, your capital gain would be $80,000 ($300,000 – ($200,000 + $50,000 – $30,000)).

Depreciation Recapture

The IRS requires its share of the tax benefit you’ve received from depreciation deductions. Upon sale, you face depreciation recapture tax on the amount of depreciation you’ve claimed (or should have claimed) over the years.

This recapture is taxed at a rate of 25%. For example, if you had $200,000 in depreciation recapture, you would owe $50,000 in taxes ($200,000 × 25%).

1031 Exchange: A Tax Deferral Strategy

A 1031 exchange allows you to defer paying capital gains tax by reinvesting the proceeds from your sale into a like-kind property. This strategy can build wealth, but it comes with strict rules:

- You must identify potential replacement properties within 45 days of selling your original property.

- You have 180 days to close on the new property.

- The replacement property should be of equal or greater value.

While a 1031 exchange can provide significant tax benefits, it’s complex. Working with a qualified intermediary ensures compliance with IRS regulations.

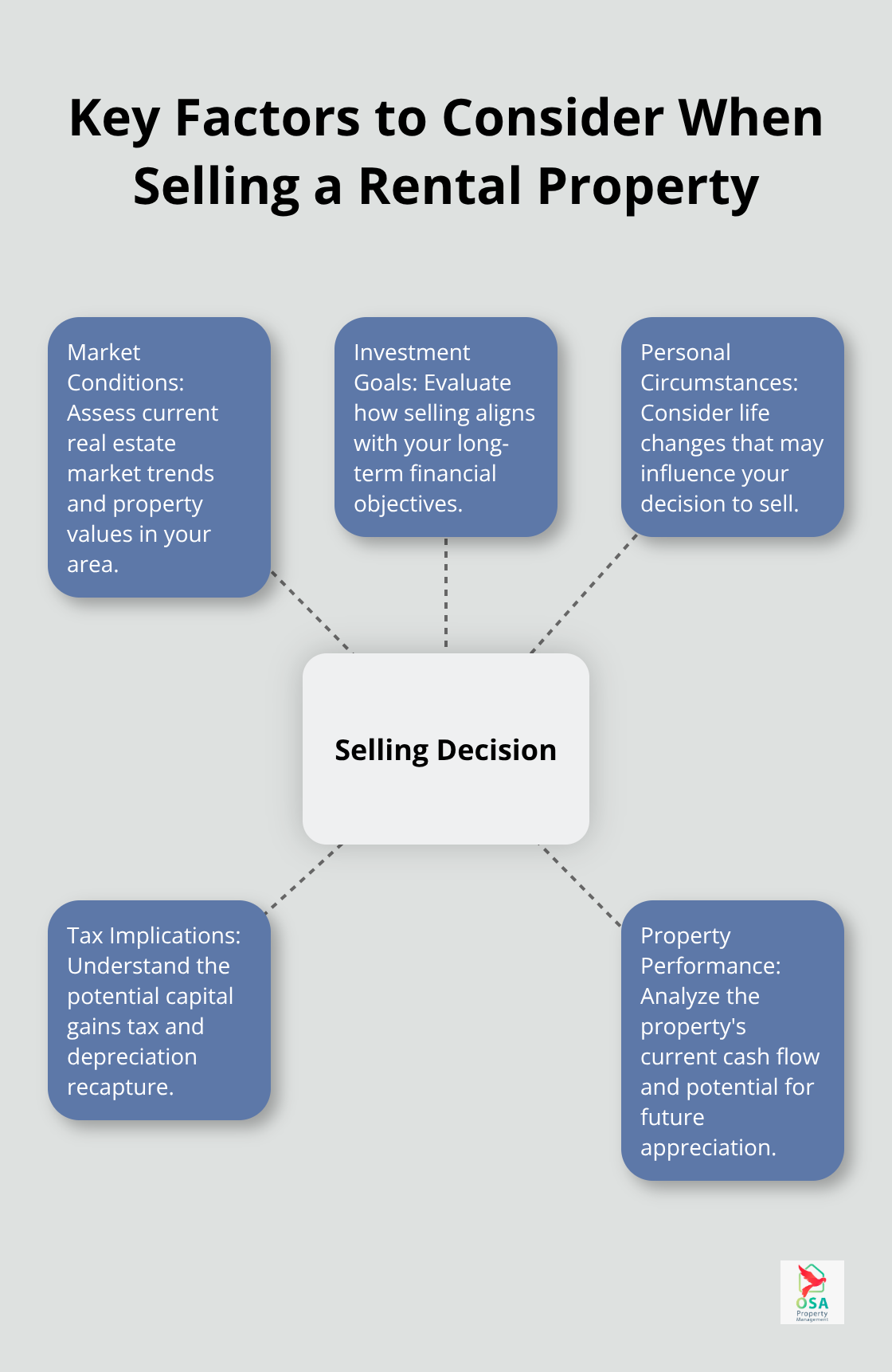

Factors Beyond Taxes

Tax considerations shouldn’t be the sole factor in your decision to sell. Market conditions, your investment goals, and personal circumstances should also play a role. Professional property management services (like those offered by Osa Property Management for Costa Rica investments) can help you navigate these decisions.

Final Thoughts

Rental properties significantly affect your taxes, offering opportunities and challenges for property owners. Proper record-keeping proves essential for effective tax management and simplifies reporting while providing crucial documentation for potential audits. The complexity of rental property taxation highlights the importance of professional guidance to navigate intricate tax laws and optimize your financial position.

Tax considerations should form part of a broader strategy aligned with your investment goals and personal circumstances. Osa Property Management offers comprehensive services to simplify property management in Costa Rica, including assistance with tax compliance. Our team can help you navigate the local real estate landscape in areas like Tarcoles, Jaco, and Manuel Antonio.

Professional advice can help you confidently manage your rental property taxes and work towards long-term financial success in real estate investing. Understanding how a rental property affects your taxes empowers you to make informed decisions and maximize your investment potential. Seek expert guidance to ensure compliance and identify strategies tailored to your unique situation.