At Osa Property Management, we know that understanding the tax benefits of rental property can significantly impact your bottom line. Owning rental properties offers numerous opportunities to reduce your tax burden and increase your overall returns.

This guide will walk you through essential deductions, strategies to maximize your benefits, and common pitfalls to avoid. By mastering these concepts, you’ll be well-equipped to optimize your rental property investments and potentially save thousands in taxes each year.

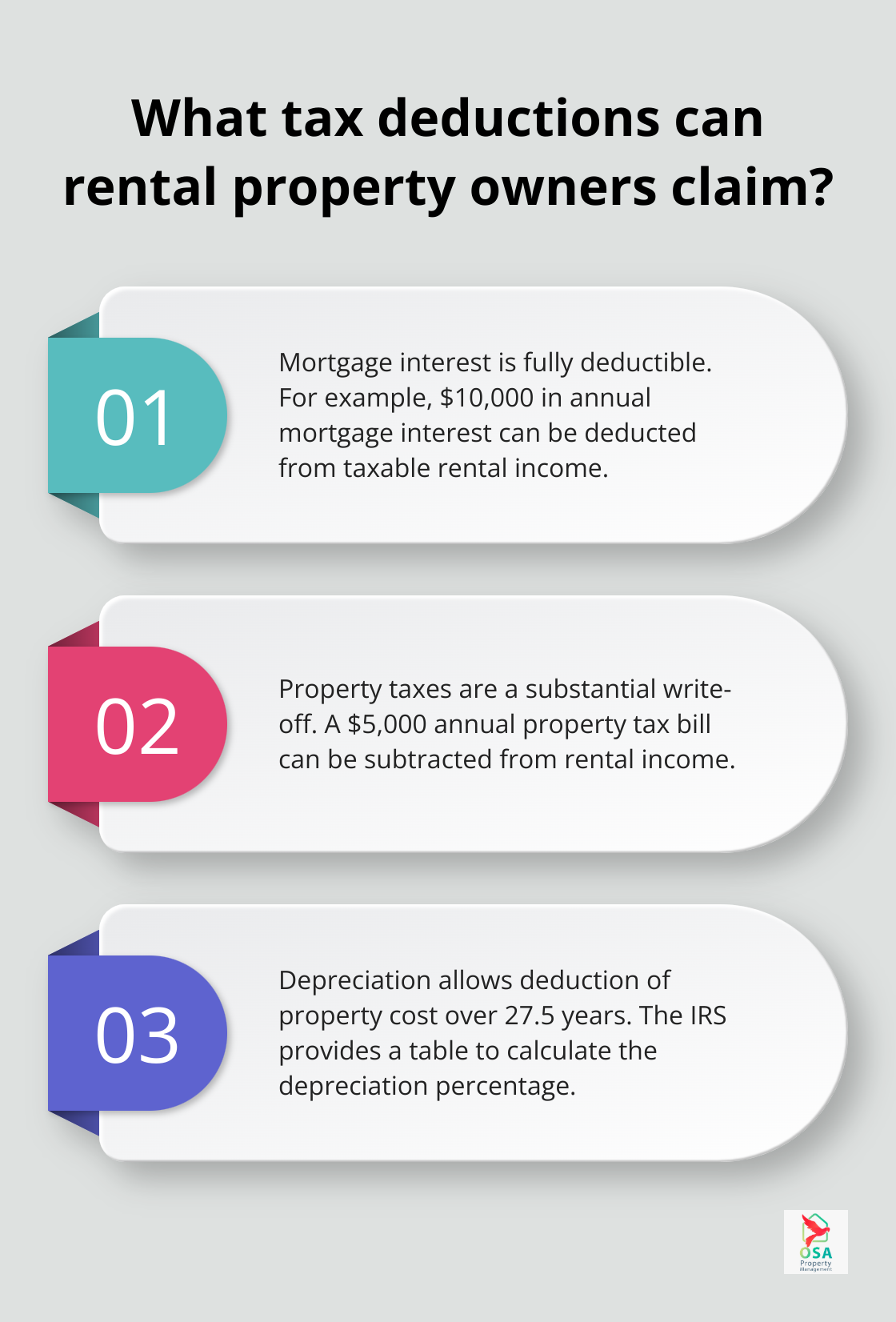

What Tax Deductions Can Rental Property Owners Claim?

Mortgage Interest: A Major Tax Advantage

Rental property ownership offers various tax benefits that can reduce your overall tax liability. One of the most significant deductions is mortgage interest. The IRS allows you to deduct the interest paid on loans used to acquire, construct, or improve your rental property. This deduction often represents a substantial amount, especially in the early years of a mortgage when interest payments are highest. For example, if you pay $10,000 in mortgage interest annually on your rental property, you can deduct $10,000 from your taxable rental income.

Property Taxes: Another Substantial Write-off

Property taxes paid on your rental property are fully deductible as a business expense. This deduction is separate from the $10,000 limit on state and local tax deductions for your personal residence. If your rental property’s annual property tax bill is $5,000, you can subtract another $5,000 from your rental income before calculating your tax liability.

Depreciation: The Silent Tax Saver

Depreciation is a powerful tax benefit that allows you to deduct the cost of your rental property over time. This means using the straight line method over a recovery period of 27.5 years. You use Table 2-2d to find your depreciation percentage.

Repairs and Maintenance: Immediate Deductions

Costs for repairs and maintenance are fully deductible in the year you incur them. This includes expenses like fixing leaky faucets, repainting, or replacing broken appliances. It’s important to distinguish between repairs and improvements. While repairs are immediately deductible, improvements must be capitalized and depreciated over time. For instance, replacing a broken window pane is a repair, but installing all new windows would be considered an improvement.

Record-Keeping: The Key to Maximizing Deductions

To truly maximize your tax benefits, you must keep meticulous records of all expenses related to your rental property. You generally must have documentary evidence, such as receipts, canceled checks or bills, to support your expenses. Keep track of any travel related to your rental property as well.

Tax laws can be complex and change frequently. While these insights provide a solid foundation, it’s always advisable to consult with a qualified tax professional for personalized advice tailored to your specific situation. They can help ensure you take advantage of all available deductions while staying compliant with current tax regulations. Now, let’s explore some strategies to further maximize your tax benefits.

How to Maximize Rental Property Tax Benefits

At Osa Property Management, we’ve observed how strategic tax planning can significantly boost returns for rental property owners. Here are some proven strategies to help you maximize your tax benefits:

Implement a Robust Record-Keeping System

The foundation of maximizing tax benefits is meticulous record-keeping. We recommend using digital tools like QuickBooks or Xero to track all income and expenses related to your rental property. These platforms allow you to categorize expenses easily, generate reports, and store digital receipts. You can create separate categories for repairs, improvements, and travel expenses, making it easier to identify deductible costs at tax time.

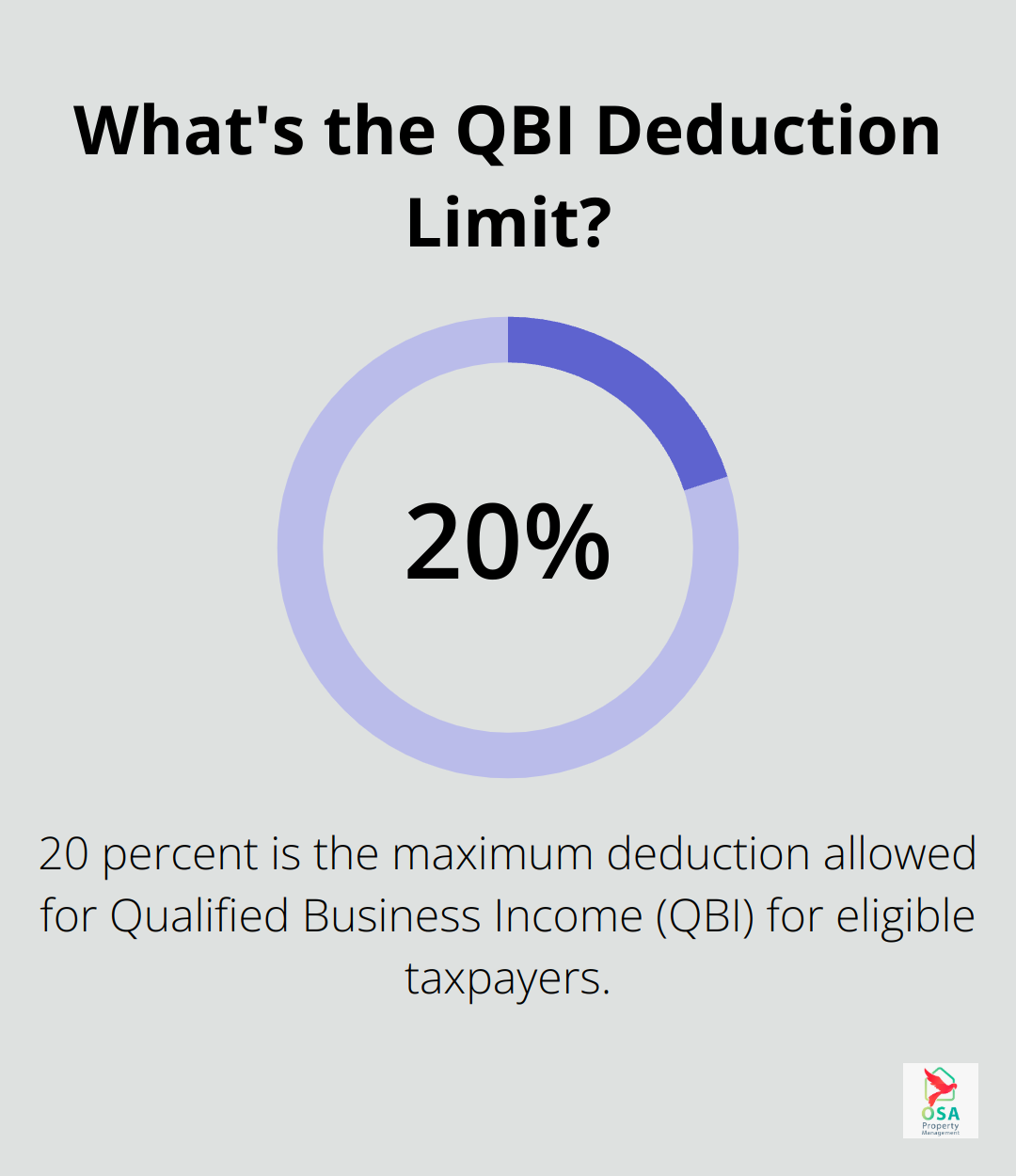

Leverage the Qualified Business Income Deduction

The Qualified Business Income (QBI) deduction allows eligible taxpayers to deduct up to 20 percent of their QBI, plus 20 percent of qualified real estate investment trust (REIT) dividends. To qualify, ensure your rental activities constitute a trade or business. This typically means you actively participate in the management of your properties for at least 250 hours per year. Keep a detailed log of your activities to support your claim if audited.

Strategically Time Income and Expenses

Timing your income and expenses can have a significant impact on your tax liability. If you expect to be in a lower tax bracket next year, consider deferring some rental income to the following year. Conversely, if you anticipate being in a higher bracket, accelerate income into the current year. For expenses, you might prepay some costs in December to increase your deductions for the current tax year. For example, paying your January mortgage payment in December could give you an extra month of interest deduction.

Explore Cost Segregation Studies

A cost segregation study can markedly improve the take-home profitability of a real estate investment. This strategy involves breaking down the components of your property and assigning shorter depreciation periods to certain elements. While the building structure is depreciated over 27.5 years, items like carpeting or appliances can be depreciated over 5-7 years. A professional cost segregation study might cost between $5,000 to $15,000, but the tax savings often far outweigh this initial investment.

Consult with a Tax Professional

Tax laws are complex and ever-changing. It’s crucial to work with a qualified tax professional who specializes in real estate investments. They can provide personalized advice tailored to your specific situation and ensure you take advantage of all available deductions while remaining compliant with current regulations. A good tax professional will help you navigate the intricacies of rental property taxation and potentially uncover additional savings opportunities you might have overlooked.

Now that we’ve covered strategies to maximize your tax benefits, let’s explore some common tax mistakes that rental property owners should avoid to ensure they’re not leaving money on the table or risking an audit.

Avoiding Common Tax Pitfalls for Rental Property Owners

Misclassifying Improvements and Repairs

Rental property owners often misclassify improvements as repairs. The IRS treats these differently. Repairs are deductible in a single year, while improvements must be depreciated over as many as 27.5 years. For example, fixing a leaky roof is a repair, but replacing the entire roof is an improvement. Misclassification can lead to audits and penalties. Try to keep detailed records of all work done on your property, including invoices that clearly describe the nature of the work.

Overlooking Deductible Travel Expenses

Many landlords don’t realize they can deduct travel expenses related to their rental property. This includes mileage for trips to collect rent, show the property to potential tenants, or perform maintenance. The IRS allows a standard mileage deduction (58.5 cents per mile for the first half of 2022 and 62.5 cents per mile for the second half). Keep a detailed log of your trips, including dates, mileage, and purpose. Even local travel can add up to significant deductions over a year.

Mishandling Security Deposits

Security deposits are often mishandled from a tax perspective. Security deposits are not income when you receive them, assuming you plan to return them to the tenant. However, if you keep part of the deposit for damages or unpaid rent, that portion becomes taxable income in the year you decide to keep it. Keep security deposits in a separate account and maintain clear records of any deductions made from these deposits.

Inadequate Documentation

Proper documentation is essential. The IRS requires taxpayers to keep records that support income and deductions claimed on tax returns. This includes receipts, canceled checks, and other documents that prove expenses. Landlords can lose thousands in deductions simply because they can’t provide adequate documentation during an audit. Consider using a digital system to store and organize your records (many apps allow you to scan and categorize receipts on the go, making tax time much less stressful).

Failing to Report All Rental Income

Some landlords make the mistake of not reporting all their rental income, especially cash payments. The IRS has ways to estimate your rental income based on fair market rents in your area. If your reported income is significantly lower, it could trigger an audit. Always report all rental income, including advance rent payments and any tenant-paid expenses.

Final Thoughts

Rental property ownership offers significant tax benefits that can reduce your tax liability and increase investment returns. Proper knowledge, meticulous record-keeping, and strategic planning allow you to optimize these advantages effectively. Professional guidance from a qualified tax expert often proves invaluable in navigating the complexities of rental property taxation and uncovering additional savings opportunities.

Effective tax planning for your rental property impacts your immediate savings and long-term financial future. Consistent application of tax principles and staying informed about law changes can help you build substantial wealth through real estate investments over time. The tax benefits of rental property ownership extend beyond immediate deductions, potentially shaping your overall financial strategy for years to come.

Osa Property Management understands the importance of maximizing returns on rental property investments in Costa Rica. Our team of experts can help you navigate property management complexities, allowing you to focus on strategic decisions that enhance your investment’s value. With our comprehensive services, we ensure your property is well-managed while you reap the financial benefits, including valuable tax advantages.