At Osa Property Management, we know that maximizing rental property tax deductions is a top priority for property owners. Navigating the complex world of tax deductions can be challenging, but it’s essential for optimizing your investment returns.

This guide will walk you through common deductions, effective record-keeping strategies, and advanced tax tactics to help you make the most of your rental property investments.

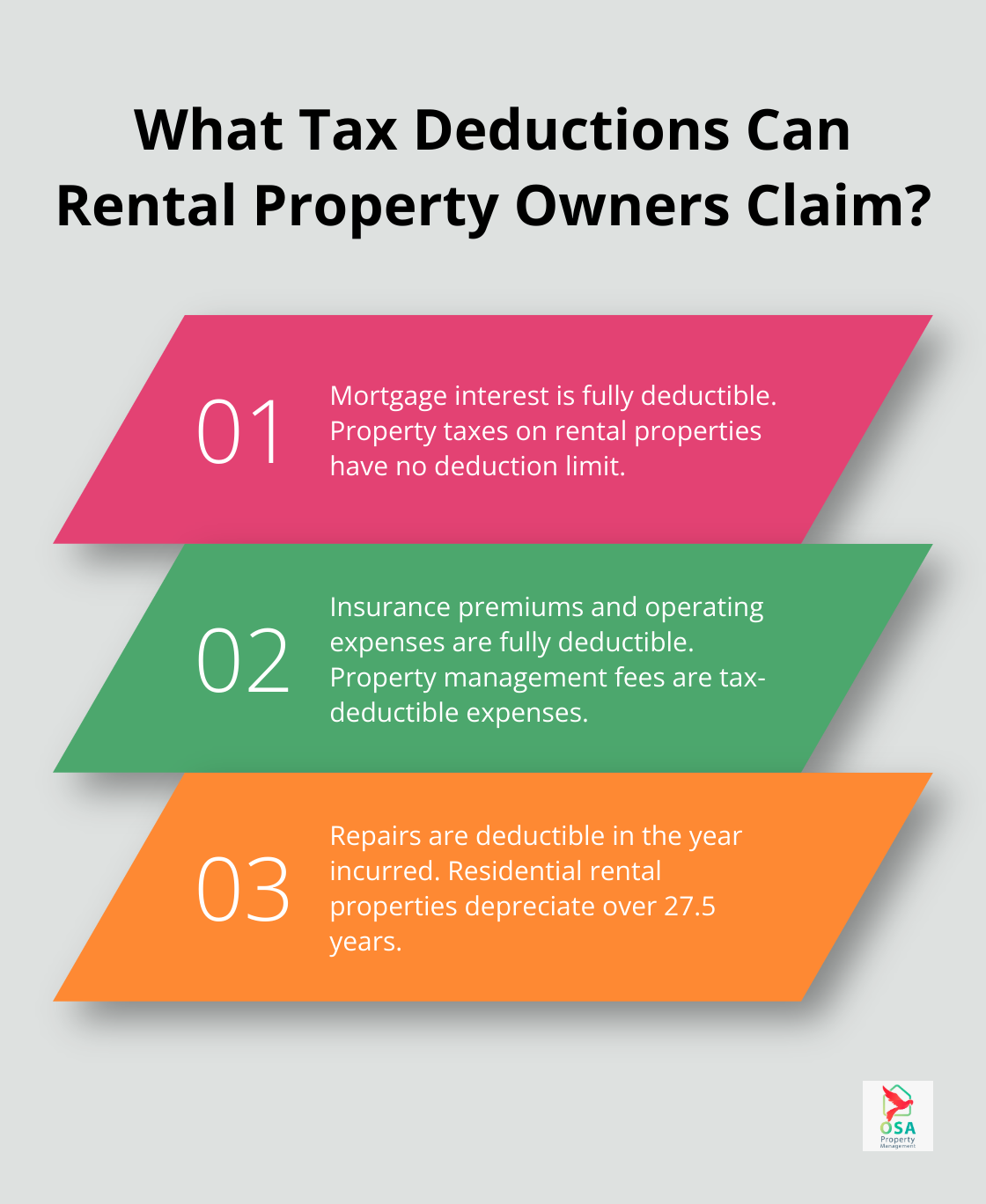

What Tax Deductions Can Rental Property Owners Claim?

Rental property owners have several tax deductions available to them that can significantly reduce their taxable income. Let’s explore some of the most common and impactful deductions you should know about.

Mortgage Interest and Property Taxes

One of the largest deductions for many property owners is mortgage interest. You can deduct the interest paid on loans used to acquire, construct, or improve your rental property. For example, if you paid $10,000 in mortgage interest last year on your rental property, that entire amount could be deductible.

Property taxes are another substantial deduction. Local and state property taxes paid on your rental property are fully deductible on your federal income tax return. However, keep in mind that the Tax Cuts and Jobs Act of 2017 placed a $10,000 cap on the total state and local tax deductions for personal residences (this limit doesn’t apply to taxes paid on rental properties).

Insurance Premiums and Operating Expenses

Insurance premiums for your rental property are fully deductible. This includes landlord liability insurance, fire, theft, and flood insurance premiums. If you paid $2,000 in insurance premiums last year, you could deduct the entire amount.

Operating expenses such as utilities that you pay for (if not covered by tenants), advertising costs for finding renters, and property management fees are all deductible. For instance, if you use a property management company, the fees you pay for their services are tax-deductible expenses.

Repairs, Maintenance, and Depreciation

Repairs and maintenance costs are generally deductible in the year you incur them. This includes painting, fixing leaks, or replacing broken windows. However, major improvements that add value to the property must be capitalized and depreciated over time.

Speaking of depreciation, this is a significant tax benefit for rental property owners. The IRS allows you to deduct the cost of your rental property over its useful life – 27.5 years for residential properties.

Professional Services and Travel Expenses

Fees paid to professionals such as attorneys, accountants, or property managers for services related to your rental property are tax-deductible. This includes costs for tax preparation, legal consultations, and property management services.

Travel expenses incurred for the purpose of checking on your property, collecting rent, or performing maintenance can also be deducted. For 2024, the standard mileage rate for the cost of operating your car, van, pickup, or panel truck increased to 67 cents a mile.

While these deductions can substantially reduce your tax liability, it’s important to keep meticulous records and consult with a tax professional. A qualified tax advisor who understands the nuances of rental property taxation can help ensure you’re claiming deductions correctly and maximizing your benefits. Now, let’s move on to discuss how proper record-keeping can further enhance your ability to maximize these deductions.

How to Keep Impeccable Records for Rental Property Tax Deductions

At Osa Property Management, we understand the importance of meticulous record-keeping for rental property owners. Proper documentation not only helps you stay organized but also maximizes your deductions and protects you in case of an audit.

The Foundation of Successful Tax Deductions

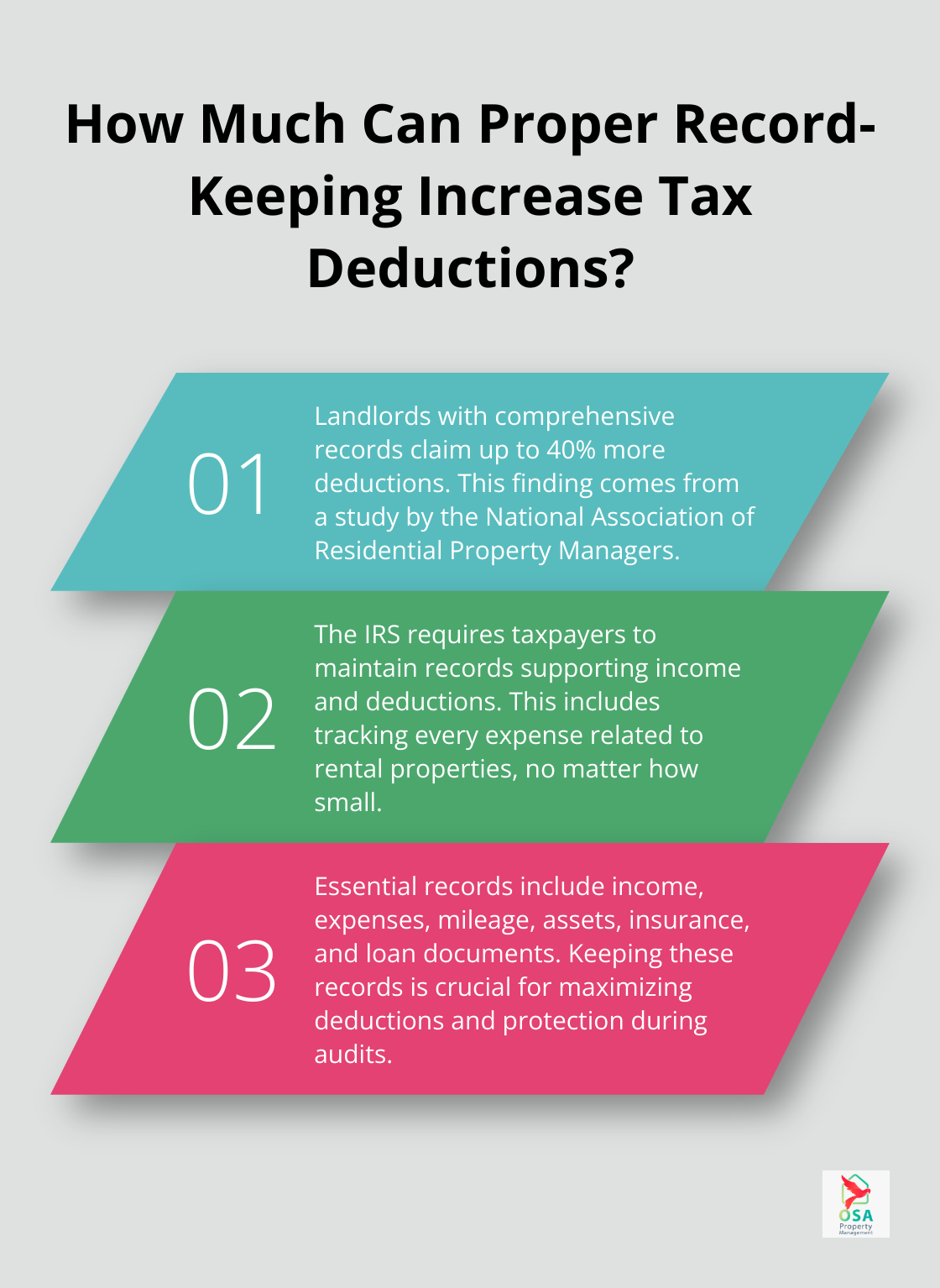

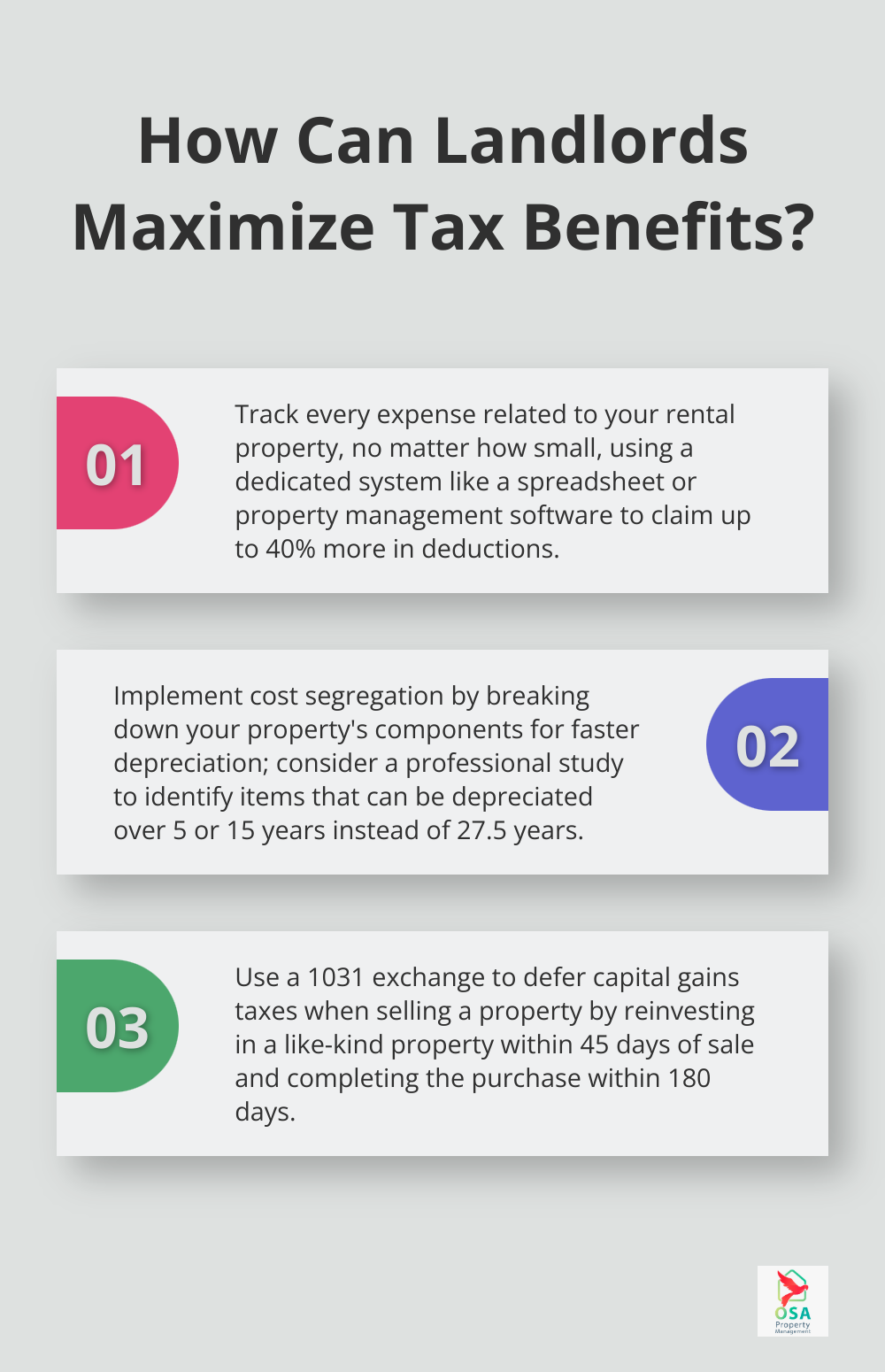

The IRS requires taxpayers to maintain records that support income and deductions claimed on tax returns. For rental property owners, this means tracking every expense related to your property. A study by the National Association of Residential Property Managers found that landlords with comprehensive records claim up to 40% more in deductions compared to those with poor documentation.

You should create a dedicated system for your rental property finances. This can range from a simple spreadsheet to sophisticated property management software. The key is consistency. Record every transaction as it occurs, no matter how small. That $5 light bulb you replaced? Log it. The $20 you spent on cleaning supplies? Note it down.

Essential Records Every Landlord Should Keep

Your record-keeping should cover several key areas:

- Income records: Rent payments, security deposits, and any other fees collected from tenants.

- Expense receipts: Everything from repair invoices to property tax statements.

- Mileage logs: If you use your personal vehicle for property-related travel.

- Asset records: Purchase documents for the property and any major improvements.

- Insurance documents: Policies and premium payments.

- Loan documents: Mortgage statements and other financing paperwork.

The IRS recommends keeping track of security deposits from year to year. This record-keeping isn’t difficult if you only own one rental property.

Leveraging Technology for Efficient Record-Keeping

Digital tools have revolutionized record-keeping for rental property owners. Property management software (like Buildium or AppFolio) can streamline your processes, allowing you to track income and expenses, store digital receipts, and generate reports with ease.

For those managing just a few properties, even a simple cloud storage solution like Google Drive or Dropbox can make a significant difference. Create folders for each property and tax year, then scan and upload your documents regularly. This not only keeps your records organized but also provides a backup in case of physical damage or loss.

The Art of Receipt Management

Receipts form the backbone of your tax deductions. You should develop a habit of immediately capturing receipt information. Many landlords find success with receipt-scanning apps (such as Expensify or Evernote). These tools allow you to snap a photo of your receipt and categorize it on the spot, reducing the chance of lost or forgotten expenses.

For digital transactions, set up email filters to automatically sort and save receipts and invoices into designated folders. This simple step can save hours of searching come tax time.

The goal is to create a system that’s easy to maintain throughout the year. Investing a little time each week in organizing your records will save you from the stress of scrambling for documentation when it’s time to file your taxes or face an audit.

Now that we’ve covered the basics of record-keeping, let’s explore some advanced tax strategies that can further optimize your rental property investments.

Advanced Tax Strategies for Rental Property Investors

Cost Segregation: Accelerate Depreciation

Cost segregation is a method of tax planning that can help real estate owners increase their cash flow. This strategy involves breaking down the cost of your property into its component parts and depreciating them over shorter periods. While the building structure depreciates over 27.5 years, certain components (like carpeting or landscaping) can depreciate over 5 or 15 years.

A cost segregation study is required to implement this strategy, which can be costly depending on the property size and complexity.

1031 Exchanges: Defer Capital Gains Tax

A 1031 exchange allows you to defer capital gains taxes by reinvesting the proceeds from the sale of one investment property into another “like-kind” property. Generally, if you make a like-kind exchange, you are not required to recognize a gain or loss under Internal Revenue Code Section 1031.

To qualify, you must identify a replacement property within 45 days of selling your original property and complete the purchase within 180 days. Work with a qualified intermediary to ensure compliance with IRS rules.

Navigate Passive Activity Loss Rules

Passive activity loss rules can limit your ability to deduct rental losses against other income. However, if you qualify as a real estate professional or your modified adjusted gross income is less than $100,000, you may deduct up to $25,000 in rental losses against your other income.

To qualify as a real estate professional, you must spend more than 750 hours per year in real estate activities and more than half of your working hours in real estate. Keep detailed time logs to prove your status to the IRS.

Home Office Deductions for Landlords

If you manage your rental properties from a home office, you may qualify for a home office deduction. The IRS allows you to deduct a portion of your home expenses based on the percentage of your home used exclusively for your rental business. This can include a portion of your mortgage interest, property taxes, utilities, and maintenance costs.

The simplified method allows you to deduct $5 per square foot of your home office (up to 300 square feet, for a maximum deduction of $1,500). Alternatively, use the regular method, which involves calculating the actual expenses attributable to your home office.

Maximize Travel Expense Deductions

Travel expenses related to your rental property business are deductible, but document them meticulously. This includes mileage for local trips to your properties, as well as longer-distance travel for property management or investment purposes.

For 2024, the standard mileage rate for business use of a personal vehicle is 67 cents per mile. Alternatively, deduct actual vehicle expenses, including gas, maintenance, and depreciation. For overnight trips, deduct lodging, meals (50% deductible), and transportation costs.

Implementing these advanced strategies requires careful planning and often professional guidance. Consult with a tax professional who specializes in real estate investments to ensure you maximize your deductions while staying compliant with tax laws.

Final Thoughts

Rental property tax deductions offer substantial benefits for property owners. Savvy investors can reduce their tax liability through various deductions, including mortgage interest, property taxes, insurance premiums, and depreciation. Meticulous record-keeping and the use of digital tools ensure the claiming of every eligible deduction.

Advanced strategies such as cost segregation studies and 1031 exchanges can further optimize tax positions. These tactics require careful planning and execution, making professional tax advice essential. A qualified tax professional who specializes in real estate investments can help navigate the intricacies of tax law and maximize deductions while maintaining compliance.

Osa Property Management understands the importance of maximizing rental property tax deductions. Our team of experts can help you navigate property management complexities in Costa Rica. We provide comprehensive services covering everything from marketing to maintenance, giving property owners peace of mind while optimizing their investments (and potential tax benefits).