Owning a rental property can be a lucrative investment, but it comes with complex tax implications. At Osa Property Management, we understand the challenges property owners face when navigating the tax landscape.

This guide will break down the essential tax considerations for rental property owners, from income and deductions to capital gains and reporting requirements. We’ll provide you with practical insights to help you make informed decisions and maximize your investment’s potential.

How Rental Income Affects Your Taxes

Defining Rental Income

Rental income encompasses more than just monthly rent payments. The IRS considers several sources as taxable rental income:

- Regular monthly rent

- Advance rent payments

- Security deposits (if kept due to lease violations)

- Property or services received in lieu of cash payments

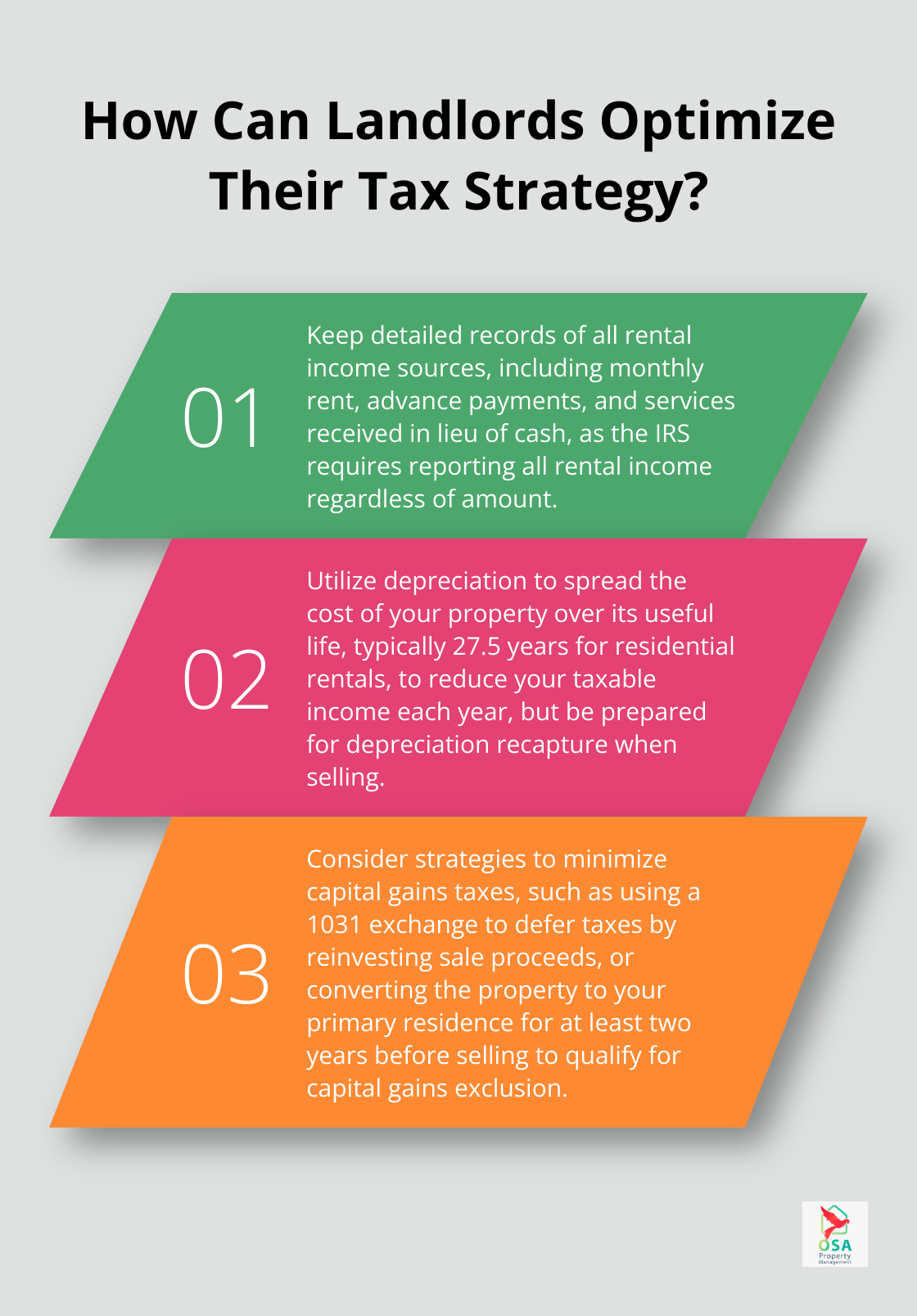

For example, if a tenant offers to paint your property instead of paying a month’s rent, you must report the fair market value of this service as rental income. The IRS requires property owners to report all rental income on their tax returns, regardless of the amount.

Deductible Expenses: Reducing Your Tax Burden

While rental income increases your tax liability, deductible expenses can offset this impact. Various credits, deductions, and incentives are available for owners of rental properties to maximize their benefits.

It’s important to note that property improvements (such as adding a new room) are not immediately deductible. These costs must be depreciated over time.

Leveraging Depreciation

Depreciation serves as a powerful tax tool for rental property owners. It allows you to spread out the cost of the property over its useful life, reducing your taxable income each year. For most residential rental properties, the IRS sets this period at 27.5 years.

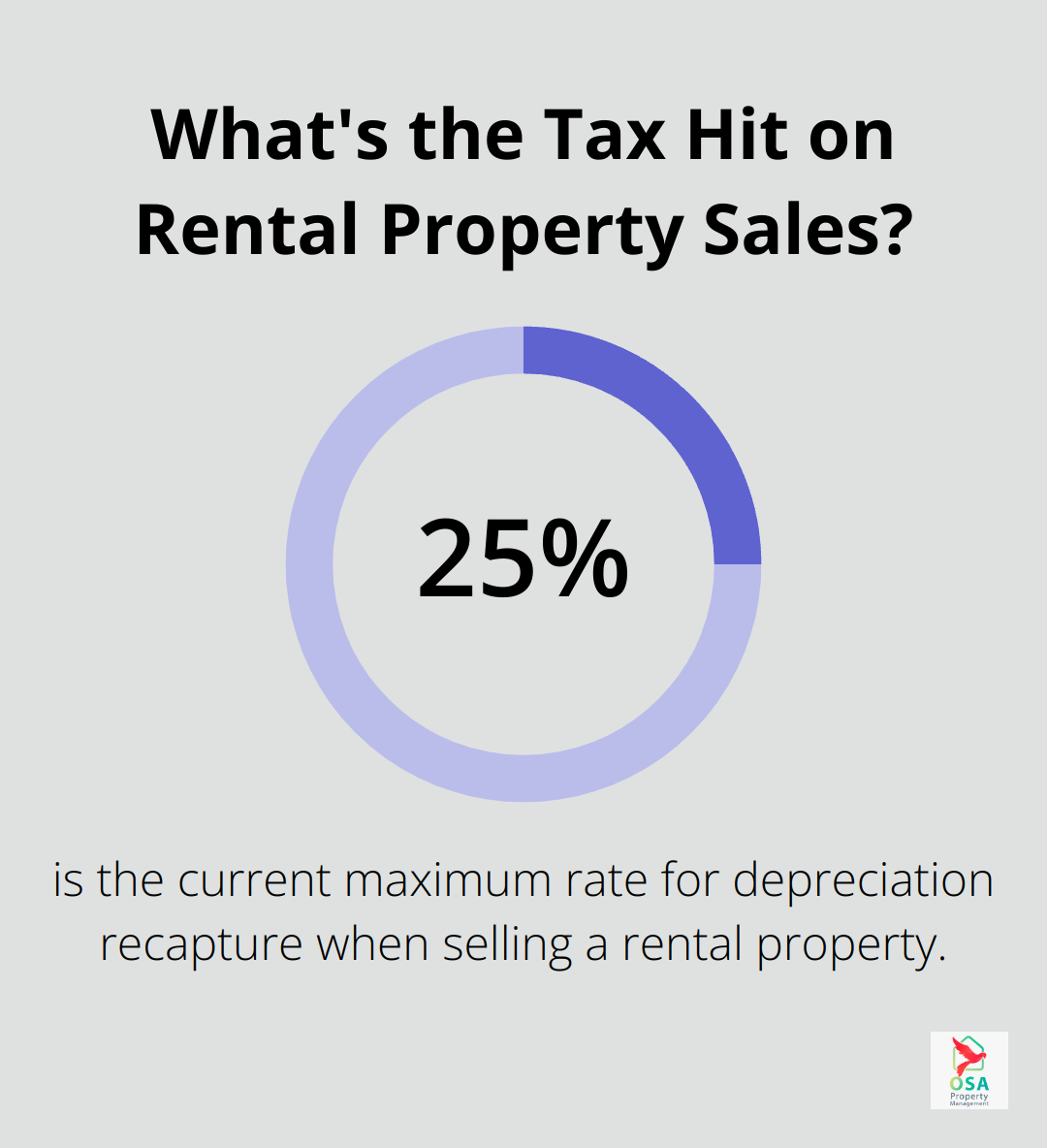

However, be aware of depreciation recapture when you sell the property. You’ll need to pay taxes on the depreciation you’ve claimed over the years, with a current maximum rate of 25%.

Tax Reporting Considerations

Accurate record-keeping is essential for rental property owners. You must maintain detailed records of all income sources and expenses to ensure proper tax reporting. The IRS recommends keeping these records for at least three years after filing your tax return.

When it comes time to file your taxes, you’ll need to report your rental income and expenses on Schedule E of Form 1040. This form allows you to calculate your net rental income or loss for the year.

Understanding these tax implications can help you make informed decisions about your rental property investments. The complexities of tax law often necessitate professional guidance. A qualified tax advisor can help you navigate the nuances of rental property taxation and ensure you maximize your deductions while staying compliant with IRS regulations.

As we move forward, let’s examine the impact of capital gains and losses on your rental property investments.

How Capital Gains Impact Your Rental Property Taxes

Understanding Capital Gains for Rental Properties

Capital gains represent the profits you make when you sell a rental property for more than its adjusted basis. The adjusted basis typically includes the original purchase price plus improvements, minus claimed depreciation. For instance, if you purchased a property for $1,500,000, invested $500,000 in improvements, and claimed $74,360 in depreciation, your adjusted basis would be $1,925,640. A sale price of $2,500,000 would result in a capital gain of $574,360.

Short-Term vs. Long-Term Capital Gains

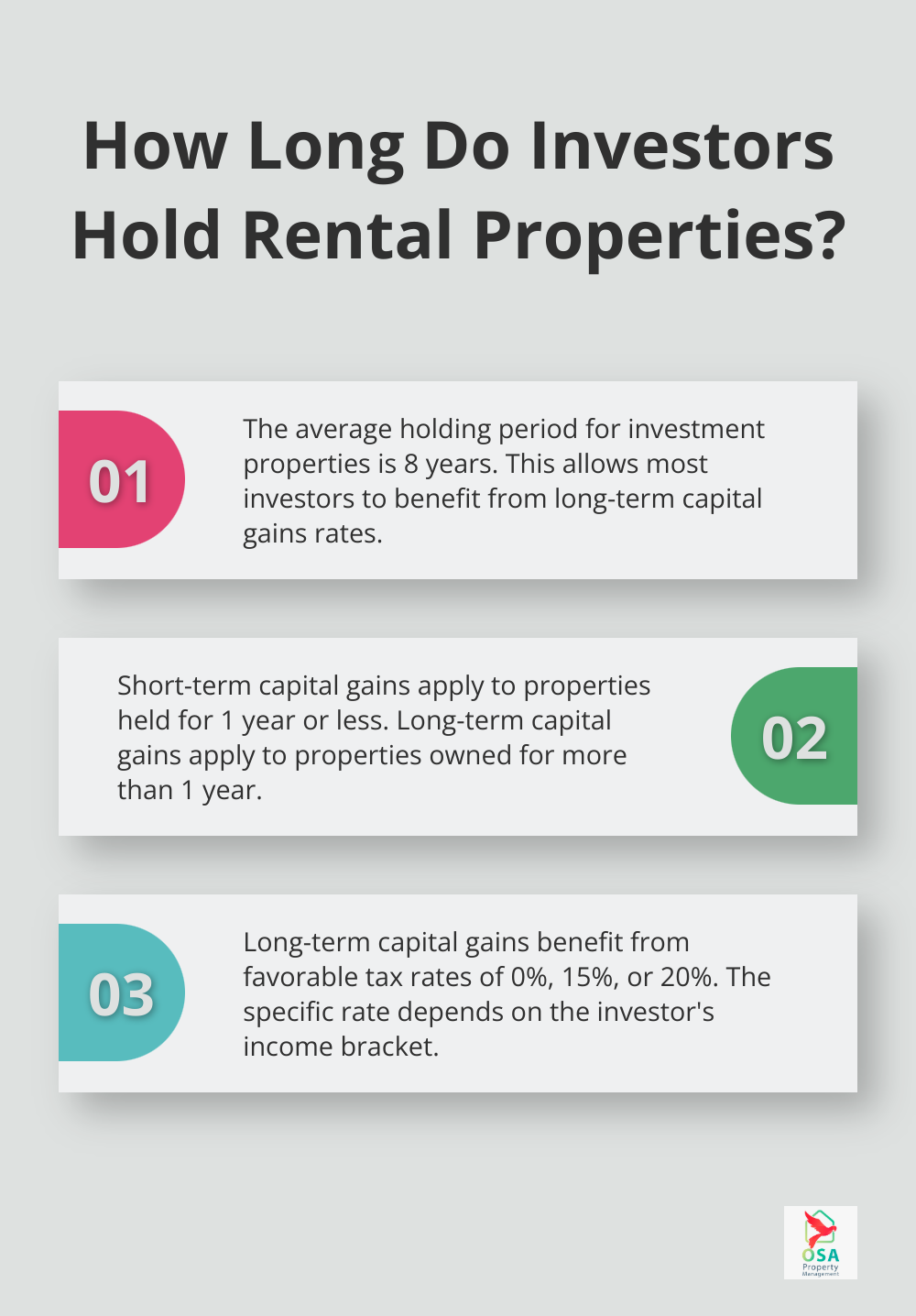

The duration of property ownership significantly affects your tax rate. Short-term capital gains apply to properties held for one year or less and incur taxes at your ordinary income tax rate. Long-term capital gains, for properties owned longer than a year, benefit from more favorable tax rates: 0%, 15%, or 20%, depending on your income bracket.

Most rental property owners can achieve substantial tax savings by holding their property for at least a year before selling. The National Association of Realtors reports that the average holding period for investment properties is approximately 8 years, allowing most investors to take advantage of long-term capital gains rates.

Strategies to Minimize Capital Gains Taxes

You can employ several strategies to reduce your capital gains tax burden:

- 1031 Exchange: This method allows you to defer capital gains taxes by reinvesting the sale proceeds into a similar property. It’s an effective tool for real estate investors who want to upgrade their portfolio without immediate tax consequences.

- Tax-Loss Harvesting: This process involves reducing tax exposure when selling a rental property by pairing the gains from the sale with the loss from another investment.

- Primary Residence Conversion: If you live in your rental property as your primary residence for at least two of the five years before selling, you may qualify for a capital gains exclusion (up to $250,000 for individuals or $500,000 for married couples).

- Installment Sales: Spreading the sale over multiple tax years can potentially keep your income in lower tax brackets, thus reducing your overall tax burden.

- Opportunity Zones: Investing your capital gains in designated Opportunity Zones provides tax benefits, including deferral and potential reduction of capital gains taxes.

Tax laws can be complex and change frequently. While these strategies can prove effective, their applicability depends on your specific situation. We recommend consulting with a tax professional to develop a tailored strategy for your rental property investments.

As we move forward, let’s examine the tax reporting requirements for rental property owners, which play a critical role in maintaining compliance and maximizing your investment returns.

Navigating Tax Reporting for Rental Properties

Schedule E: Your Rental Income and Expense Report

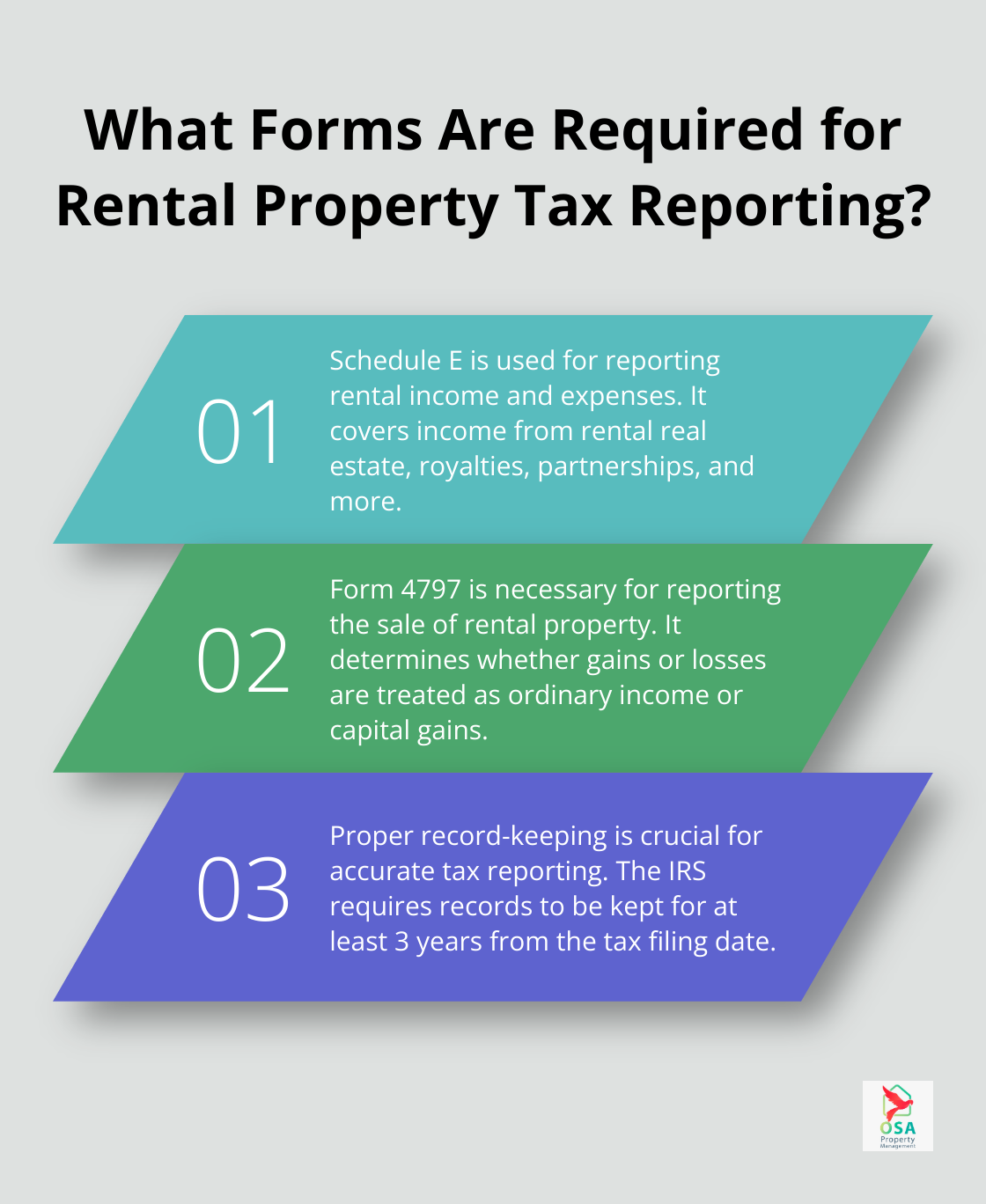

Schedule E (Form 1040) forms the cornerstone of rental property tax reporting. This form is used to report income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, and residual interests. You must report all rental income received during the tax year, including rent payments, advance rent, and any other fees collected from tenants.

On the expense side, you can deduct various costs associated with your rental property. Common deductions include mortgage interest, property taxes, insurance premiums, maintenance costs, and property management fees. Don’t forget to include depreciation, which we discussed earlier.

The IRS scrutinizes Schedule E closely, so accuracy is paramount. Use accounting software specifically designed for rental properties to track income and expenses throughout the year. This practice simplifies the process of filling out Schedule E and reduces the risk of errors.

Form 4797: Reporting Property Sales

When you sell a rental property, you must report the transaction on Form 4797. This form is used to report the sale of business property, including rental real estate. The information you provide on Form 4797 determines whether your gain or loss is treated as ordinary income or capital gain.

A critical aspect of Form 4797 is reporting depreciation recapture. The IRS requires you to report the gain including any depreciation recapture required by sections 1245 and 1250 as it would otherwise be reported if you were not making the election.

To complete Form 4797 accurately, you need records of your original purchase price, any improvements made to the property, and all depreciation claimed during your ownership. This underscores the importance of maintaining detailed records throughout your ownership period.

Best Practices for Record-Keeping

Proper record-keeping forms the foundation of accurate tax reporting. The IRS requires you to keep records that support your income and deductions for at least three years from the date you file your tax return. However, we recommend keeping records for the entire period of ownership plus an additional three years.

Essential records to maintain include:

- Purchase documents and closing statements

- Receipts for all improvements and repairs

- Mortgage statements and property tax bills

- Insurance policies and premium payments

- Rental agreements and tenant communications

- Bank statements showing rent deposits and expense payments

Consider using a cloud-based storage system to keep digital copies of all these documents. This practice not only helps with organization but also provides a backup in case of physical document loss.

Try to conduct monthly reconciliations of your rental income and expenses. This habit helps catch discrepancies early and makes year-end tax preparation much smoother.

Tax reporting for rental properties can be complex, but with proper planning and record-keeping, it doesn’t have to overwhelm you. If you’re unsure about any aspect of your tax reporting, consult with a tax professional who specializes in real estate investments. Their expertise can help you navigate the complexities of rental property taxation and ensure you maximize your deductions while staying compliant with IRS regulations.

Final Thoughts

Owning a rental property and taxes involves complex considerations, but understanding key aspects can lead to significant financial benefits. Rental income, including advance payments and non-cash compensations, is taxable. However, numerous deductions can offset this income, such as mortgage interest, property taxes, and depreciation.

Capital gains tax implications play a pivotal role in long-term investment strategies. Accurate and timely tax reporting is essential for rental property owners. Familiarizing yourself with forms like Schedule E and Form 4797 ensures compliance and maximizes tax benefits.

At Osa Property Management, we understand the challenges of managing rental properties in Costa Rica. Our team can assist you with various aspects of property management, including tax compliance and financial reporting. You can focus on growing your investment while we handle the day-to-day operations and ensure your property remains a valuable asset in your portfolio.