Managing rental property accounting in Costa Rica can be complex, but it’s essential for success in the vacation rental market. At Osa Property Management, we understand the challenges property owners face when navigating local tax laws and financial reporting requirements.

This guide will walk you through the key components of rental property accounting in Costa Rica and provide practical tips to streamline your processes. By implementing these strategies, you’ll be better equipped to maintain accurate financial records and maximize your rental property’s profitability.

Why Accurate Rental Accounting Matters in Costa Rica

Navigating Costa Rica’s Tax Landscape

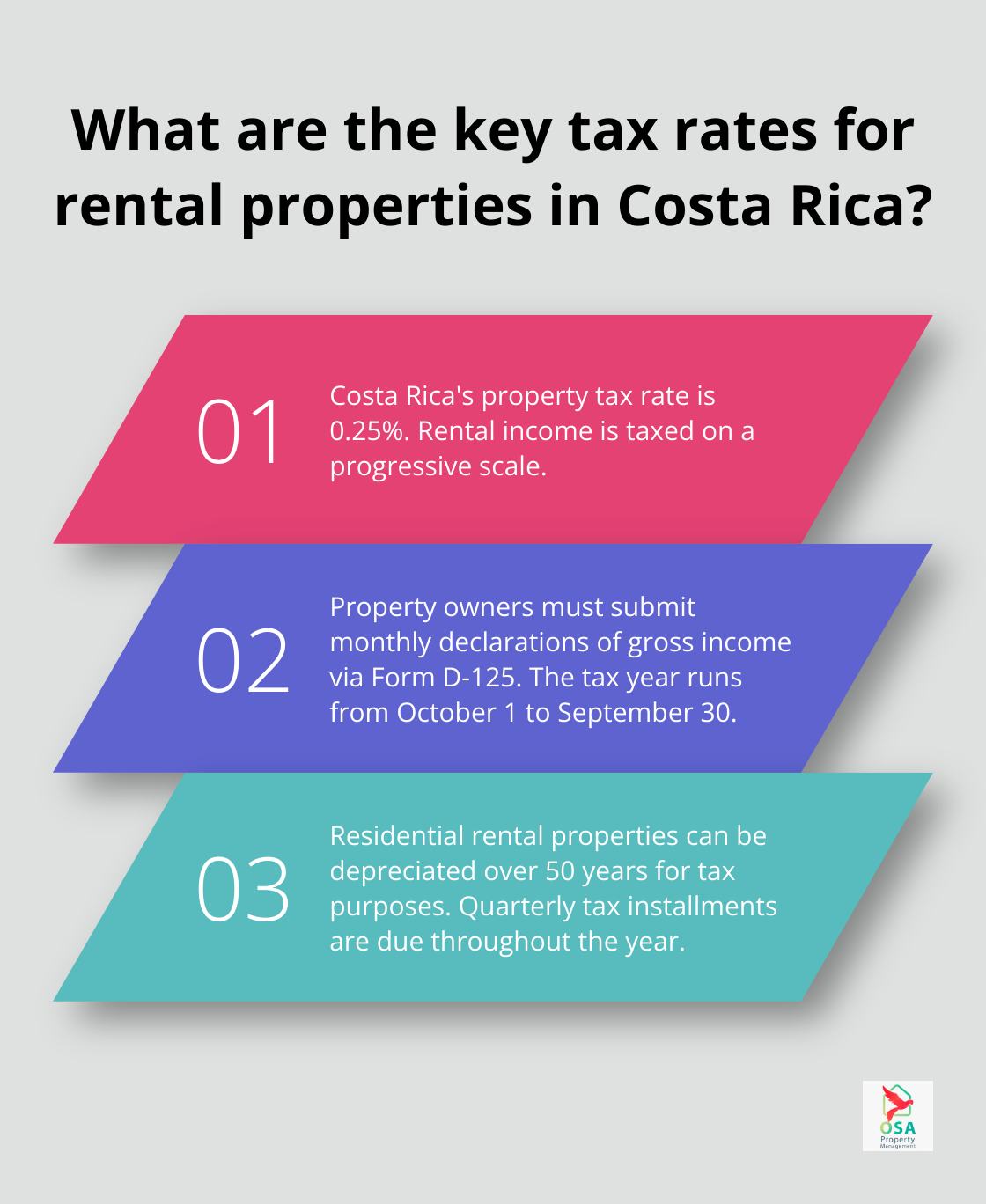

Costa Rica’s tax system for rental properties presents a complex landscape. Property owners must report rental income and pay taxes on a progressive scale. As of 2025, rental income follows a progressive tax rate structure. Costa Rica’s property tax rate of 0.25% is relatively low, but property owners must still navigate the complexities of income tax on rental earnings.

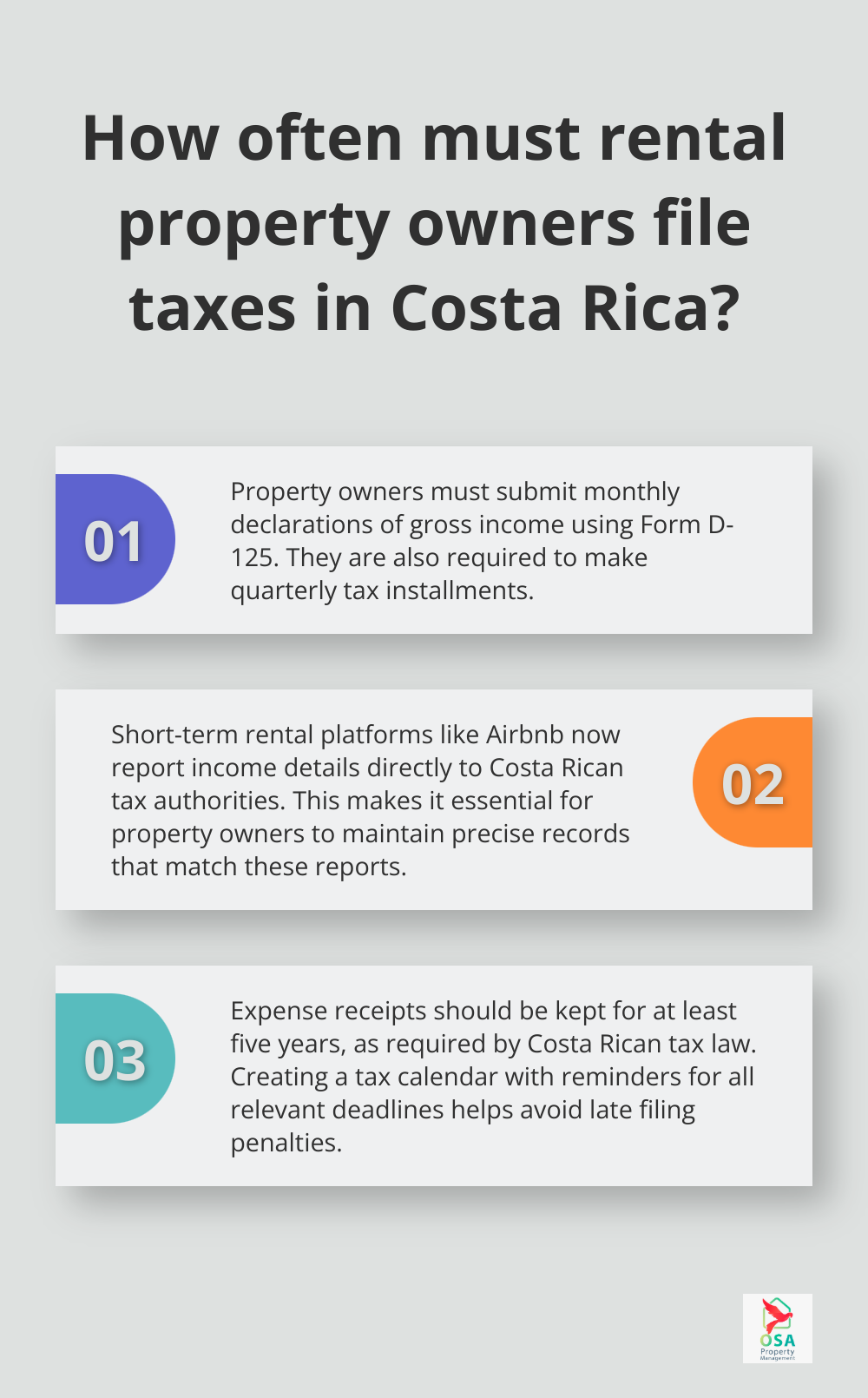

To maintain compliance, property owners must submit monthly declarations of gross income via Form D-125. This requirement simplifies the annual tax filing process but demands consistent attention to detail. The Costa Rican tax year spans from October 1 to September 30, with quarterly tax installments due on specific dates throughout the year.

Financial Clarity for Informed Decision-Making

Accurate accounting provides a clear picture of your rental property’s financial health. It allows you to track income streams, categorize expenses, and understand your property’s profitability. This level of financial transparency proves essential for making informed decisions about your investment.

Meticulous expense tracking helps identify areas where costs can decrease or where investments might improve your property’s appeal to renters. You’ll also position yourself to set competitive rental rates that balance profitability with market demand.

Maximizing Deductions and Minimizing Tax Liability

Proper accounting practices enable property owners to take full advantage of available tax deductions. Costa Rican tax law allows for various deductible expenses, including maintenance costs, management fees, utilities, and mortgage interest. Moreover, residential rental properties can depreciate over 50 years, providing a valuable tax deduction opportunity.

Accurate recording of these expenses and understanding the tax implications can significantly reduce taxable income. This approach not only ensures compliance but also maximizes the financial benefits of your rental property investment.

Avoiding Legal Issues and Penalties

Failure to maintain precise accounts can lead to severe penalties and legal issues in Costa Rica. The country’s tax authorities (such as the Dirección General de Tributación) have become increasingly vigilant in enforcing compliance. As of December 2024, new requirements for short-term rental properties are being established to ensure high standards of safety, quality, and tax transparency.

Non-compliance with Costa Rican rental income reporting can result in significant fines. These penalties not only impact your bottom line but can also damage your reputation as a property owner.

Streamlining Financial Management

Accurate rental accounting streamlines your overall financial management process. It allows you to:

- Set up a separate bank account for rental activities, simplifying income and expense tracking.

- Use digital accounting software (like QuickBooks Online or Xero) to streamline documentation.

- Evaluate the tax implications of rental types (long-term vs. short-term) for tax efficiency.

- Accelerate deductible expenses in the current tax year to manage income tax bracket impacts.

As we move forward, we’ll explore the essential components of Costa Rica rental accounting, providing you with the tools to maintain accurate financial records and optimize your property’s performance.

Key Elements of Rental Accounting in Costa Rica

Effective rental accounting in Costa Rica requires a comprehensive approach that covers several important aspects. We’ve identified four key elements that form the foundation of successful rental property financial management.

Income Tracking

Accurate income tracking is the foundation of rental accounting in Costa Rica. This involves recording all revenue streams, including long-term leases, short-term rentals, and any additional services provided to tenants. For short-term rentals, platforms like Airbnb now report income details directly to Costa Rican tax authorities, making it essential to maintain precise records that match these reports.

We recommend using specialized property management software that integrates with booking platforms to automatically record income. This approach minimizes errors and saves time. Additionally, setting up a dedicated bank account for rental activities simplifies income tracking and helps separate personal and business finances.

Expense Categorization

Proper expense categorization is vital for maximizing tax deductions and understanding your property’s financial performance. Common expense categories for Costa Rican rental properties include maintenance, utilities, property management fees, insurance, and mortgage interest.

To streamline this process, we advise using digital tools for receipt management. Apps like Expensify or Receipt Bank allow you to capture and categorize expenses on the go, ensuring no deductible costs are overlooked. Try to keep original receipts for at least five years, as required by Costa Rican tax law.

Financial Reporting

Generating property-specific financial statements provides a clear picture of each rental unit’s performance. These reports should include profit and loss statements, balance sheets, and cash flow analyses.

For multi-property owners, we recommend creating separate reports for each property to identify which units are performing well and which may need attention. This granular approach allows for more informed decision-making about property improvements, rental rates, and potential sales.

Tax Preparation

Tax preparation in Costa Rica requires ongoing attention due to monthly and quarterly filing requirements. Property owners must submit monthly declarations of gross income (via Form D-125) and make quarterly tax installments.

To stay ahead of these obligations, we suggest creating a tax calendar with reminders for all relevant deadlines. This proactive approach helps avoid late filing penalties, which can be substantial in Costa Rica.

Additionally, staying informed about tax law changes is important. The Costa Rican government occasionally updates tax regulations, and being aware of these changes can help you optimize your tax strategy. Consider subscribing to updates from the Dirección General de Tributación or working with a local tax professional to stay current.

Implementing these key elements of rental accounting will provide a solid foundation for managing your Costa Rican rental property finances. However, navigating the complexities of local tax laws and accounting practices can be challenging. That’s why many property owners choose to work with experienced property management companies (like Osa Property Management). These experts can handle all aspects of rental accounting, ensuring compliance and maximizing your property’s financial performance. In the next section, we’ll explore practical strategies to streamline your rental accounting process and make it more efficient.

How to Streamline Your Rental Accounting Process

Embrace Cloud-Based Accounting Software

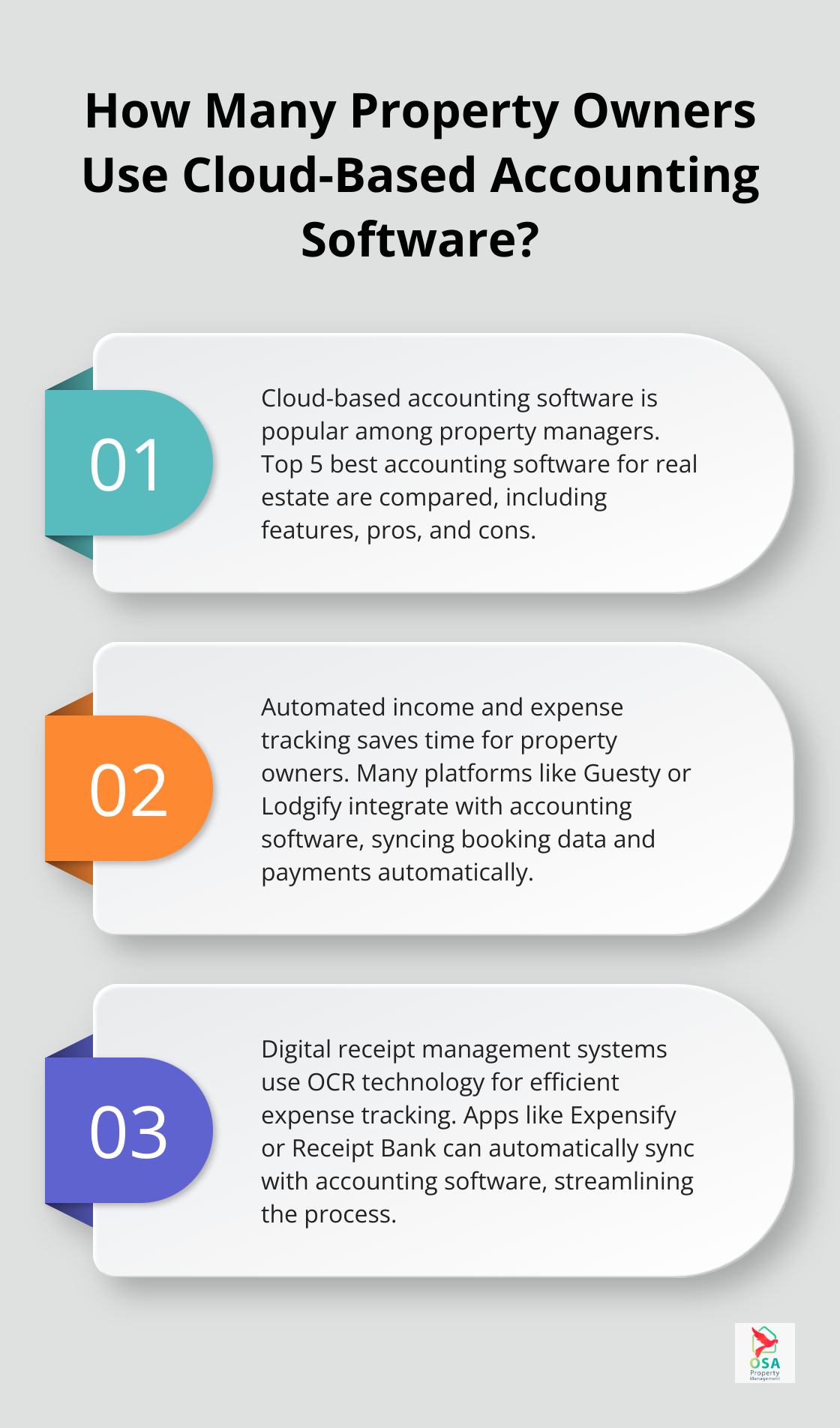

Embrace Cloud-Based Accounting Software tailored for property management. These platforms offer free comparisons of the top 5 best accounting software for real estate, listing out key features, pros and cons, and website information. This can help you choose the right software to track income, categorize expenses, and generate financial reports, making it easier to stay on top of your rental property finances.

Automate Income and Expense Tracking

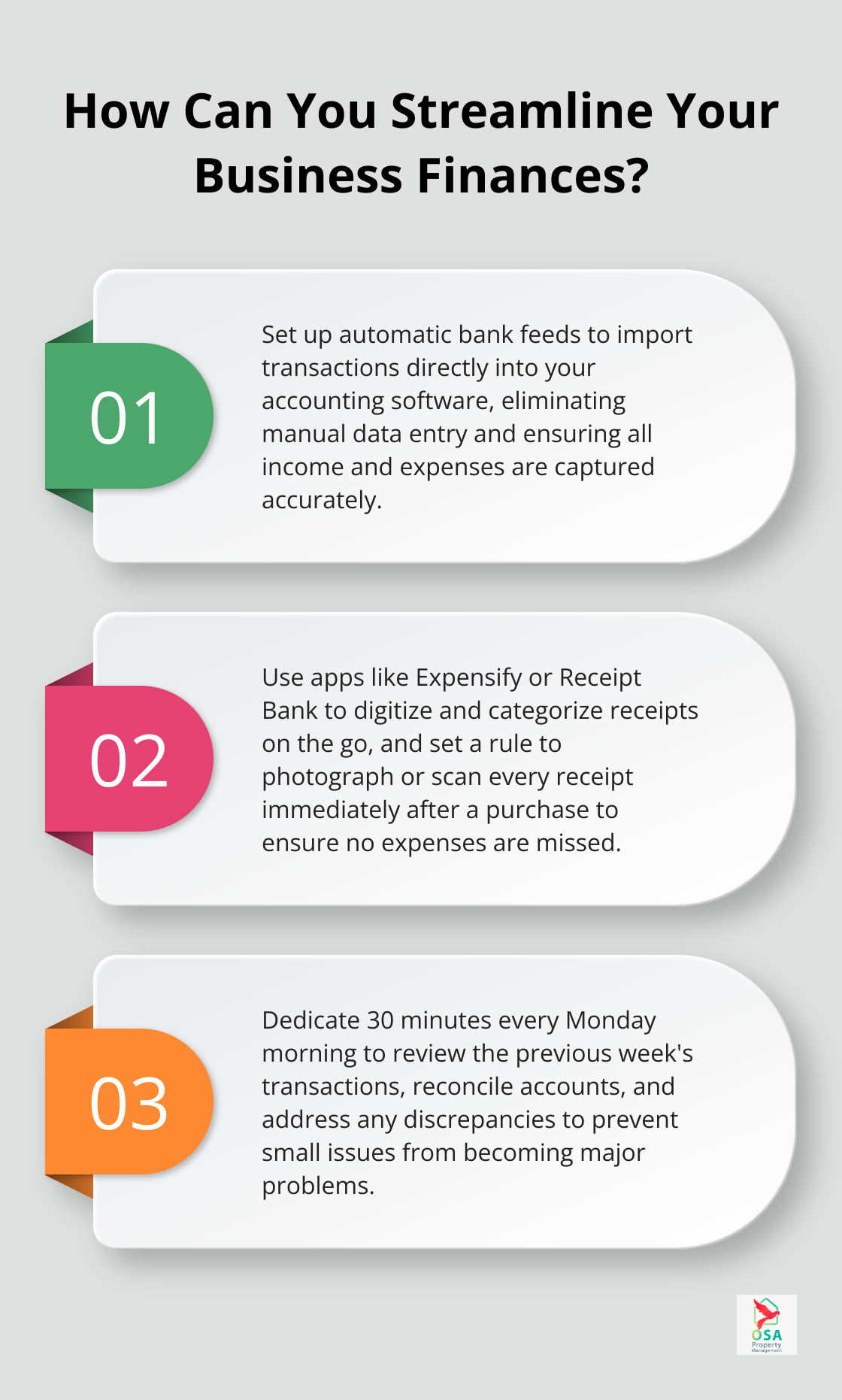

Set up automatic bank feeds to import transactions directly into your accounting software. This eliminates manual data entry and ensures all income and expenses are captured accurately. Many property management platforms (like Guesty or Lodgify) integrate with accounting software, automatically syncing booking data and payments.

If you use Airbnb for short-term rentals, you can connect it directly to your accounting software. This way, every booking and payout is automatically recorded, saving time and reducing the risk of missed transactions.

Implement a Digital Receipt Management System

Use apps like Expensify or Receipt Bank to digitize and categorize receipts on the go. These tools use OCR technology to extract key information from receipts and can automatically sync with your accounting software.

A practical tip: Set a rule to photograph or scan every receipt immediately after a purchase. This habit ensures no expenses slip through the cracks and makes tax time much less stressful.

Establish a Weekly Bookkeeping Routine

Consistency is key in rental accounting. Set aside a specific time each week to review transactions, reconcile accounts, and address any discrepancies. This regular check-in prevents small issues from becoming major problems.

Try to spend 30 minutes every Monday morning reviewing the previous week’s transactions. This routine helps catch any unusual expenses or missing income promptly, allowing for quick resolution.

Leverage Local Expertise

Leverage Local Expertise for unmatched experience and tenure in property management. Specialists in Property Management, Vacation Rental, Marketing, Finance, and Service can provide invaluable assistance in navigating specific tax laws and regulations. Consider partnering with a local accountant or property management company familiar with the nuances of rental property accounting in your area.

Professional property management services can handle everything from monthly declarations to annual tax filings, ensuring full compliance while maximizing deductions. These experts stay up-to-date with the latest tax regulations, providing peace of mind for property owners.

Final Thoughts

Rental property accounting in Costa Rica requires a strategic approach to ensure success in the vacation rental market. Property owners must implement user-friendly accounting software, establish consistent bookkeeping routines, and utilize digital tools for receipt management. These practices streamline financial processes and maintain compliance with local tax regulations.

Accurate income tracking, proper expense categorization, and regular financial reporting provide valuable insights into property performance. These insights enable informed decision-making and maximize profitability. However, navigating Costa Rica’s complex tax landscape can challenge foreign property owners.

Professional property management services can make a significant difference in handling rental property accounting and tax compliance. Osa Property Management offers expert assistance in all aspects of rental property management (including accounting). Their team ensures property owners enjoy the benefits of their investment without the stress of day-to-day management.