Owning rental property in Costa Rica comes with tax obligations that confuse many investors. We at Osa Property Management help property owners navigate CR rents taxation basics so they can keep more of what they earn.

This guide covers the tax rates, deductions, and common mistakes that cost investors thousands of dollars each year.

How Rental Income Gets Taxed in Costa Rica

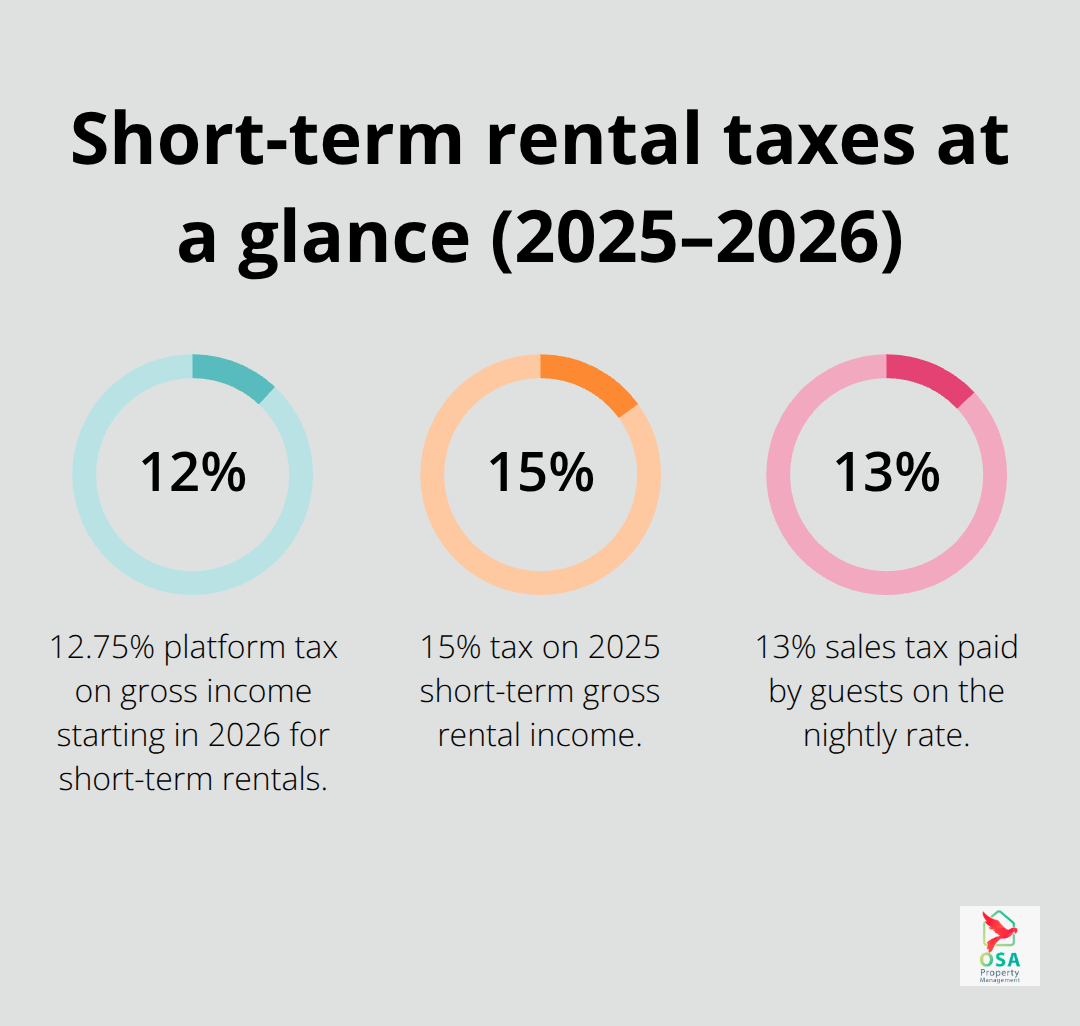

Costa Rica taxes rental income progressively based on your total annual earnings, not on individual properties. Long-term rental income attracts tax rates of 10% if you earn between 3.8 and 5 million colones annually, 15% for 5 to 7.5 million colones, 20% for 7.5 to 10 million colones, and 25% for anything above 10 million colones. Two investors with identical properties will pay vastly different tax rates depending on their total income. Short-term rentals through platforms like Airbnb and Booking.com operate under different rules entirely. Starting in 2026, short-term rental income from platforms faces a new 12.75% tax on gross income, and properties must be registered to avoid penalties. For 2025, short-term rentals are taxed at 15% of gross rental income with a 15% expense deduction allowed. Additionally, vacation rental guests pay 13% sales tax on top of the nightly rate, which you must remit monthly using Form D-104.

The distinction between long-term and short-term rental classifications matters enormously because your tax bracket can shift dramatically depending on which model you use.

Your Residency Status Changes Your Tax Obligations

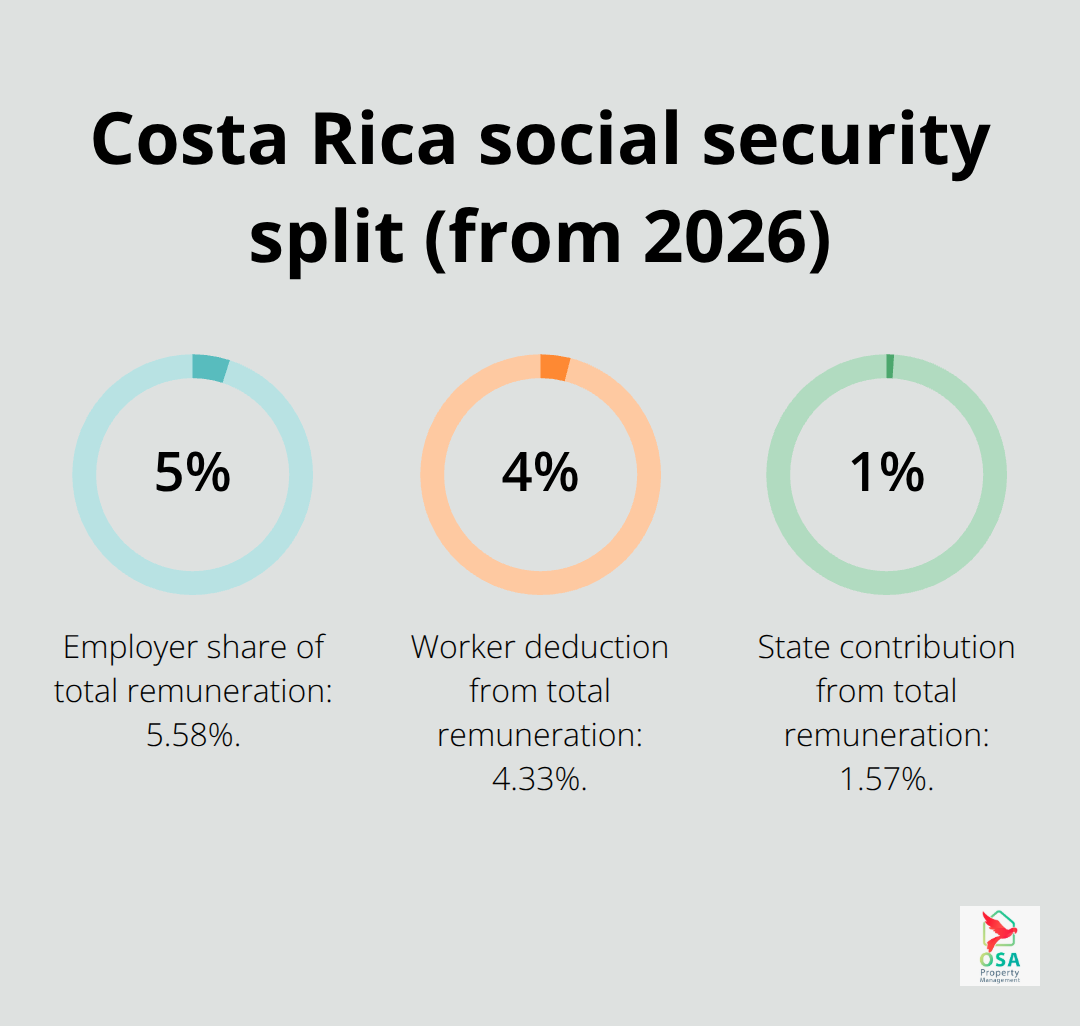

Non-residents and residents face identical rental income tax rates in Costa Rica, but your residency status affects social security obligations and how you file taxes. As a non-resident, you must grant power of attorney to a local attorney or legal team to file required disclosures since digital signature cards are restricted to Costa Rican citizens and residents. As a resident, you handle filings directly but must navigate the social security system. Starting in 2026, social security contributions rise to 11.66% of total remuneration, split between employer (5.58%), worker (4.33%), and state (1.57%).

If you employ staff for property management or maintenance, these costs increase your operating expenses significantly.

Electronic Invoicing and Tax Authority Oversight

Electronic invoicing became mandatory on October 1, 2018, meaning every rental transaction must generate a factura electrónica recorded with tax authorities. This system allows the Ministerio de Hacienda to cross-check your declared rental income against platform records and tenant payments, making underreporting nearly impossible. The tax authority uses these electronically issued invoices to verify that rental income matches what you report on your tax filings. Platforms hosting short-term rentals must register with tax authorities under 2026 rules; non-registration can trigger penalties. This enforcement mechanism has tightened compliance across the rental market, and property owners who fail to report all rental income face significant consequences.

What Rental Expenses Actually Reduce Your Costa Rica Tax Bill

Maintenance and Repairs That Count as Deductions

The tax authority in Costa Rica allows you to deduct legitimate business expenses from your rental income before calculating what you owe, but many property owners claim deductions they shouldn’t and miss others that would save them money. Maintenance and repairs are fully deductible, including roof repairs, plumbing fixes, painting, and appliance replacements, but only if they restore the property to working condition rather than improve it beyond its original state. Capital improvements like adding a new deck or upgrading to luxury finishes cannot be deducted in the year you spend the money. Keep detailed receipts and invoices for every maintenance expense because the Ministerio de Hacienda scrutinizes rental income claims heavily, and electronic invoicing requirements mean your contractors’ records are already in the system.

Management Fees and Professional Services

Management fees paid to a professional property management firm are fully deductible, which reduces your taxable income while ensuring compliance with electronic invoicing rules and monthly tax filings. If you self-manage, you cannot deduct a salary for yourself, but you can deduct costs for accounting software, property management platforms, and professional fees for tax preparation or legal advice. These professional services (accounting, legal, and tax preparation) stack up quickly and represent real money back in your pocket at tax time.

Mortgage Interest, Insurance, and Property Costs

Mortgage interest on loans used to purchase or improve rental property is deductible, but principal payments are not, so separate these carefully on your statements. Property insurance premiums, liability coverage, and theft protection all qualify as ordinary business expenses. Utilities that you cover for tenants, internet costs if included in rent, and property taxes are also deductible from your rental income.

What the Tax Authority Rejects

Personal expenses disguised as rental costs-such as meals, entertainment, or vehicle costs for personal use-trigger audits and penalties. The tax authority cross-references your declared expenses against platform records and bank statements, so inflated or fabricated deductions are discovered quickly. Document everything with electronic invoices, bank transfers, and receipts that match your tax filings. Many investors lose thousands annually by either claiming improper deductions that invite scrutiny or failing to document legitimate expenses that would reduce their tax bracket.

The line between what reduces your tax bill and what invites an audit depends entirely on documentation and honesty. Understanding which expenses qualify sets you up to avoid costly mistakes when filing your annual returns.

Mistakes That Cost You Thousands in Rental Taxes

The Ministerio de Hacienda has tightened enforcement on rental properties across Costa Rica, using electronic invoicing records and platform data to cross-check what you report versus what you actually earn. Many property owners lose substantial money annually through three preventable errors that trigger audits, penalties, or missed deductions.

Underreporting Rental Income Invites Severe Penalties

The first mistake is underreporting rental income, which happens far more often than you might think. Platforms like Airbnb and Booking.com now report their data directly to tax authorities, and your tenant payment records are already in the system through electronic invoicing requirements. The Ministerio de Hacienda will discover the discrepancy within months and assess penalties on unreported income. Non-residents must grant power of attorney to a local attorney to file disclosures, and residents must file directly, but both face identical enforcement. The tax authority cross-references your declared income against platform records and bank statements already recorded electronically, so underreporting is discovered quickly.

Claiming Personal Expenses as Business Deductions

The second major error involves claiming personal expenses as business deductions to inflate your deductible costs artificially. Vehicle expenses for personal use, meals, entertainment, or home office supplies that benefit your household rather than the rental operation invite immediate audit flags. The tax authority cross-references your declared expenses against bank statements and contractor invoices already recorded electronically, so fabricated or exaggerated deductions are discovered quickly. Legitimate expenses like mortgage interest, property insurance, maintenance costs, and management fees are fully deductible and can shift your income into a lower tax bracket, but only if documented properly with electronic invoices and bank transfers that match your tax filings.

Misunderstanding Residency Status and Its Tax Impact

Your residency status creates the third costly mistake when investors misunderstand how it affects their filing obligations and social security contributions. Non-residents and residents pay identical rental income tax rates, but residents who employ staff for maintenance or management must account for rising social security contributions that reach 11.66% of total remuneration starting in 2026 (split between employer contributions of 5.58%, worker deductions of 4.33%, and state contributions of 1.57%). Many non-resident investors fail to maintain their power of attorney arrangements or file required digital disclosures through a local legal team, leading to penalties and liens on their properties. The National Registry database tracks whether your property taxes and rental compliance are current, and lenders or buyers will discover unpaid obligations during due diligence. Residency also affects how you access deductions and whether you can claim certain professional services expenses. A resident who hires an accountant to manage electronic invoicing and monthly Form D-104 sales tax filings can deduct those costs, while a non-resident must have their attorney or legal team handle these filings and can deduct the legal fees. The distinction matters because your total tax obligation depends on understanding which expenses reduce your taxable income within your specific residency category. Property owners who address these three mistakes typically drop one or two tax brackets immediately, saving thousands of colones annually while maintaining compliance with the Ministerio de Hacienda.

Final Thoughts

Costa Rica’s rental taxation system rewards property owners who understand the rules and punishes those who ignore them. The CR rents taxation basics boil down to three realities: your income bracket determines your tax rate, the Ministerio de Hacienda electronically tracks every rental transaction, and legitimate deductions shift you into a lower tax bracket when you document them properly. Long-term rental income faces tax rates from 10% to 25% depending on your total earnings, short-term rentals face a new 12.75% platform tax starting in 2026, and mandatory electronic invoicing means the tax authority will discover underreported income or inflated deductions.

Non-residents must maintain power of attorney arrangements with a local legal team, while residents handle filings directly but face rising social security contributions that reach 11.66% starting in 2026 if they employ staff. You should document every expense with electronic invoices and bank transfers, separate mortgage interest from principal payments, and claim only legitimate business costs like management fees, property insurance, and maintenance repairs. If you employ staff or manage multiple properties, calculate your social security obligations now rather than facing surprises at tax time.

Professional guidance matters because the difference between claiming deductions correctly and incorrectly can mean thousands of colones annually. We at Osa Property Management handle electronic invoicing, monthly tax filings, and compliance with the Ministerio de Hacienda for property owners across the southern Pacific zone, and our team can help you navigate your rental tax obligations so you keep more of what your rental property earns.