Rental tax compliance in Costa Rica isn’t optional-it’s a legal requirement that affects your bottom line. Many landlords miss deductions worth thousands of dollars simply because they don’t know what qualifies.

We at Osa Property Management have helped countless property owners navigate these rules and keep more of what they earn. This roadmap walks you through everything you need to know.

How Much Tax Do You Actually Owe on Rental Income

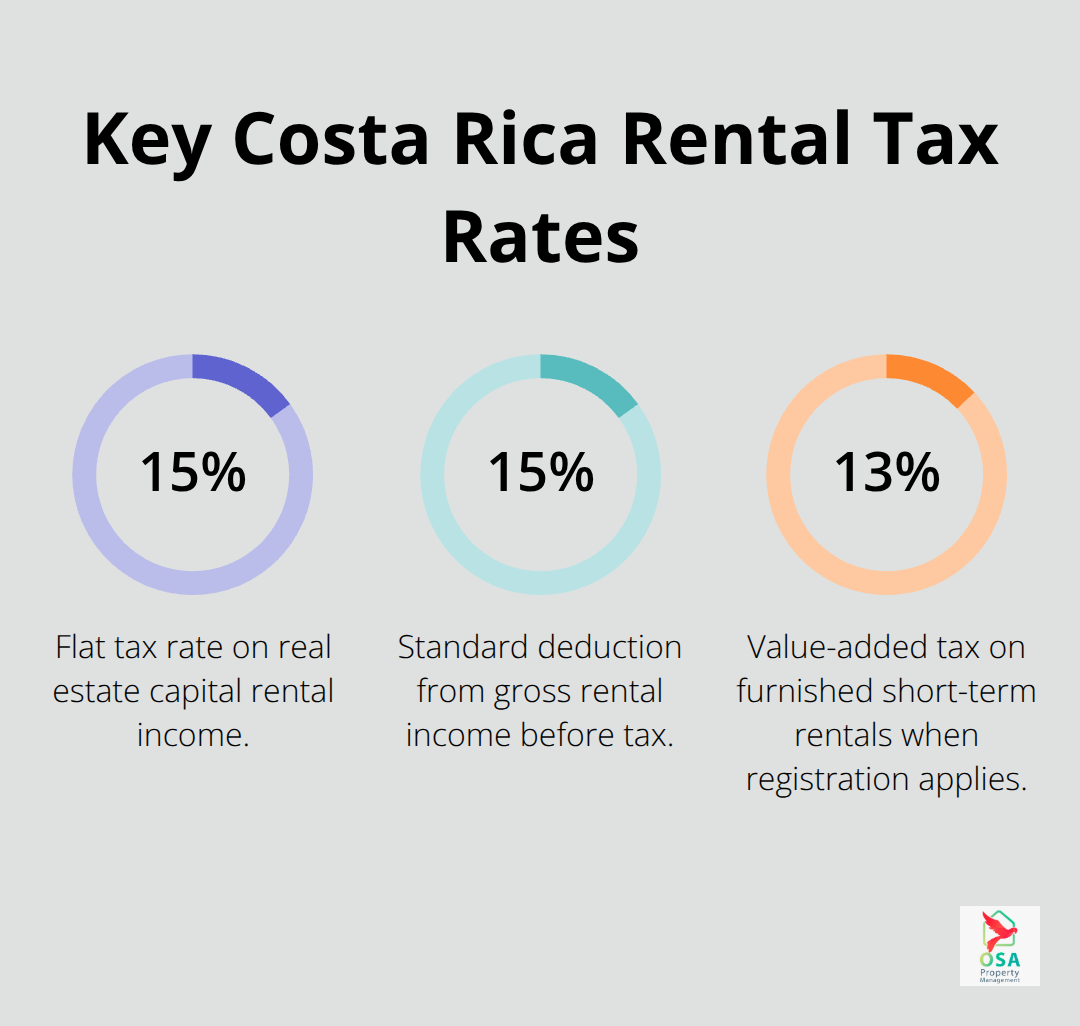

Rental income in Costa Rica is taxed at a flat 15% rate on the remaining 85% of gross rental receipts after a standard 15% deduction. This differs fundamentally from how many landlords expect taxation to work. The tax authority treats rental income as real estate capital income, not ordinary business income, and this distinction matters for how you file and what you can deduct. You must file an annual real estate capital income return with Costa Rica’s tax authority, Hacienda, to report all rental receipts. The good news is that while you cannot deduct individual expenses from the taxable base, you receive a standard deduction of 15% of your gross rental income automatically. For a property that generates 2 million colones annually in rent, that 15% standard deduction reduces your taxable base to 1.7 million colones, lowering your actual tax bill to about 255,000 colones instead of 300,000 colones.

Filing Deadlines and What Hacienda Expects

You must declare your rental income annually on the real estate capital income return, and you cannot delay this filing without facing penalties. Many landlords miss the deadline because they underestimate how long it takes to gather documentation or they assume that property managers handle all reporting automatically-they do not. You need to submit proof of all rental income you received during the tax year, including advance rent payments, lease cancellation fees, and any tenant-paid expenses that benefit you. If a tenant pays your utilities or repairs directly, that amount counts as rental income. You should keep electronic invoices for every transaction through your short-term rental platform or direct lease agreements. Non-resident foreign owners face an additional 2.5% withholding tax obligation that the buyer must deduct from the purchase price when you eventually sell the property, so you should understand your residency status now to prevent surprises later. Monthly record-keeping prevents the scramble to reconstruct a year’s worth of transactions in December. You should document everything in a dedicated business account and use accounting software that produces reports compatible with Hacienda’s electronic filing system.

The 15% Deduction Is Fixed-Not Flexible

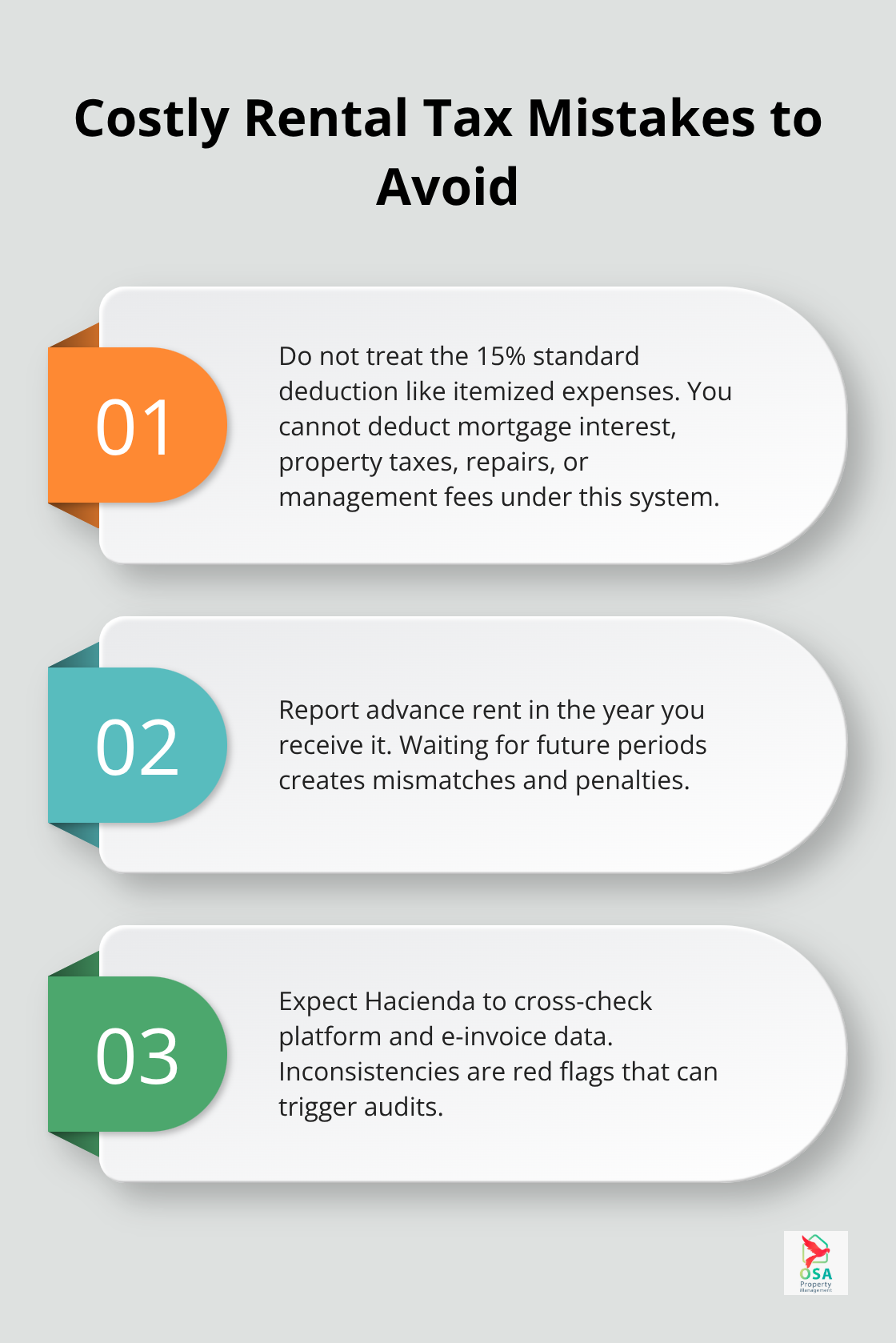

The most expensive mistake we see is treating the 15% standard deduction as if you can claim itemized expenses instead. You cannot deduct mortgage interest, property taxes, repairs, or management fees from the 15% flat rate-that deduction is fixed regardless of your actual expenses.

Some landlords waste time and money trying to claim individual deductions they will never receive. Another critical error is failing to report advance rent in the year you receive it, even if the lease covers future periods. Hacienda uses electronic invoicing records and platform data to cross-check your filings, and mismatched amounts trigger audits.

Corporate Structures and VAT Complications

If you operate through a Costa Rican corporation rather than personally, you must file a shareholders declaration for corporate rental property ownership under Law 8683, with penalties ranging from about 2,000 to 79,000 dollars for noncompliance. Many owners skip this filing because they do not realize it is mandatory for corporate structures. Additionally, furnished short-term rental properties may trigger VAT registration requirements if you exceed certain revenue thresholds, adding a 13% tax on top of your rental income tax. A local accountant experienced in Costa Rican rental taxation can clarify whether your structure requires VAT registration and help you avoid these costly surprises.

Why Professional Help Pays for Itself

Operating without professional guidance is the third major mistake landlords make. A local accountant experienced in Costa Rican rental taxation costs far less than penalties or missed deductions, and they ensure you register correctly with Hacienda from the start. They also navigate the differences between personal ownership and corporate structures, handle shareholders declarations on time, and alert you to VAT thresholds before they apply. The complexity of Costa Rica’s rental tax system-with its flat 15% rate, standard deductions, withholding obligations, and platform cross-checks-makes professional support not just helpful but practical. Your next step is to identify which filing structure fits your situation and connect with a qualified accountant who can set up your compliance system properly.

What Expenses Actually Reduce Your Rental Tax Bill

The 15% Deduction Does Not Match Your Real Costs

Costa Rica’s tax system awards you a flat 15% deduction on gross rental income, but that deduction rarely reflects what you actually spend maintaining and operating your property. The gap between that fixed deduction and your real expenses creates a significant financial problem that most landlords overlook. You cannot claim individual deductions like mortgage interest, property taxes, repairs, or management fees against your taxable rental income under the standard system. The IRS recognizes that rental property owners in the United States can deduct mortgage interest, property tax, operating expenses, repairs, and depreciation as ordinary and necessary expenses on Schedule E reporting. Costa Rica’s system works differently because it treats rental income as capital income, not business income. This structural difference means you should not waste hours tracking individual expenses hoping to reduce your 15% standard deduction. Instead, focus your energy on understanding whether your actual situation qualifies for alternative tax treatment or whether a corporate structure with the old system makes financial sense for your portfolio.

The Old System Transforms Your Tax Calculation

If you operate through a Costa Rican corporation and have employees, you can elect the old system that taxes net income annually instead of the new 15% flat rate system. This election transforms the entire calculation. Under the old system, you subtract all legitimate operating expenses from gross rental income before calculating tax, which can dramatically lower your taxable base if your property requires significant maintenance, management, or financing costs. A property that generates 2 million colones annually with 800,000 colones in documented expenses owes tax only on 1.2 million colones instead of 1.7 million colones under the standard 15% deduction system. The difference amounts to roughly 75,000 colones in additional tax liability under the flat-rate approach. Property management fees, maintenance contracts, utility invoices, HOA payments, and repair costs all qualify as deductible expenses under the old system if you have proper electronic invoices through factura electrónica.

Documentation Determines Your Deduction Success

The tax authority cross-checks invoices against Hacienda’s electronic filing system, and mismatched or undocumented expenses trigger audits. You must maintain electronic invoices for every deductible expense you claim, and the invoices must match your tax filings exactly. Contractors issue electronic invoices for repairs and maintenance work, utility companies provide digital records, and HOA administrators can supply electronic documentation of fees. Your decision between the two systems requires professional guidance from a Costa Rican tax advisor who understands your specific property costs, corporate structure, and long-term portfolio goals. The complexity of comparing actual expenses against the flat 15% deduction means that professional support pays for itself through tax savings alone.

How to Build a Tax System That Actually Works

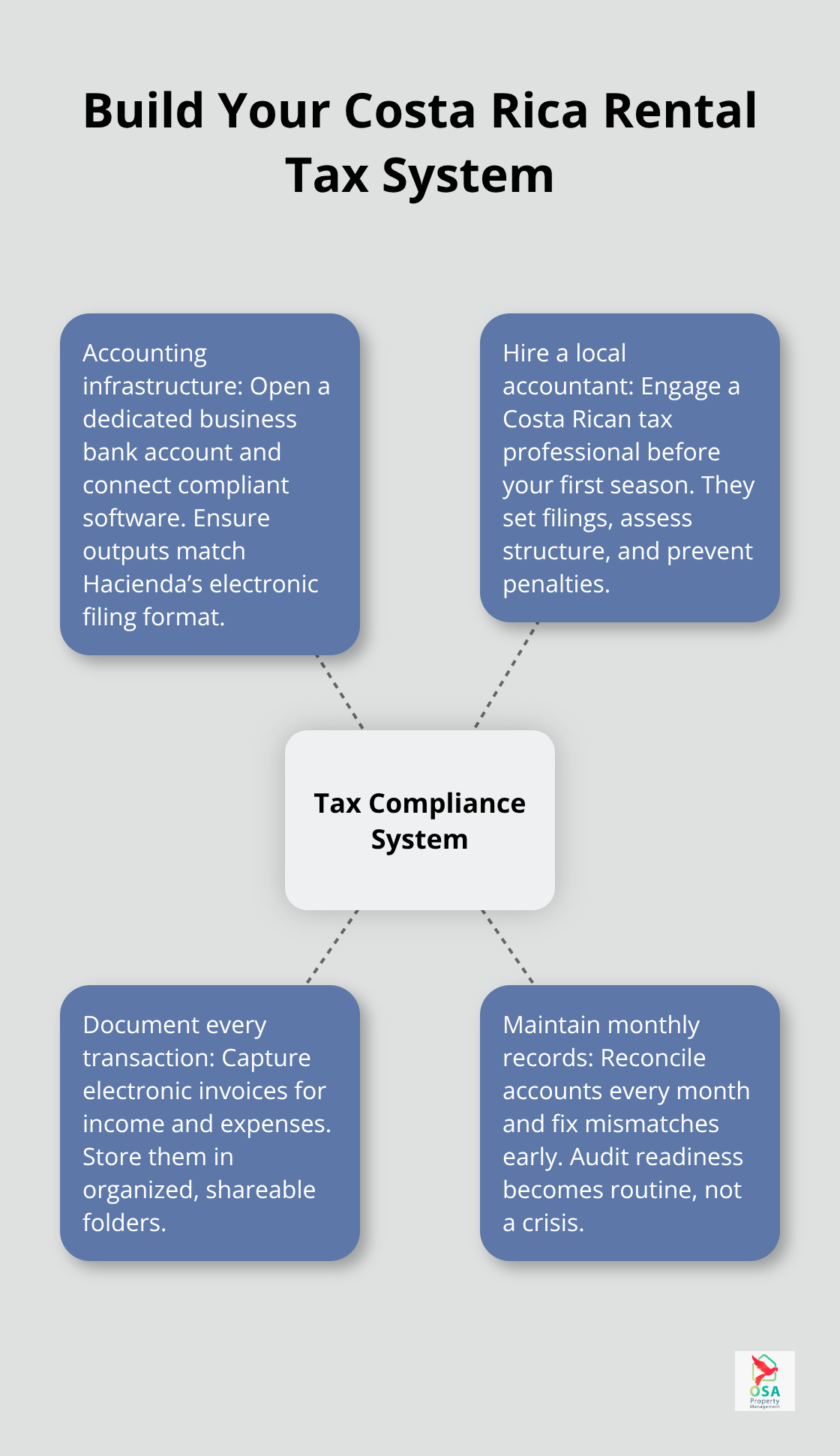

Your rental income tax compliance rests on three concrete actions: setting up accounting infrastructure that matches Hacienda’s requirements, hiring a local accountant who understands Costa Rican rental taxation, and organizing your records so thoroughly that an audit becomes a routine verification rather than a crisis.

Open a Dedicated Business Bank Account

Start with a dedicated business bank account separate from your personal finances. Open an account in Costa Rica under your tax identification number, or if you operate through a corporation, under the corporate tax ID. Every rental payment deposits into this account, and every deductible expense (if you qualify under the old system) withdraws from it.

Use accounting software that produces reports compatible with Hacienda’s electronic filing format. Most local accountants recommend software like Contabilidad or Xero configured for Costa Rican tax reporting, which automatically categorizes transactions and produces the real estate capital income return your tax authority requires. Monthly reconciliation takes 30 minutes if you stay current, but annual reconstruction takes weeks. The difference between monthly discipline and annual scrambling determines whether you catch errors before filing or discover them during an audit.

Hire an Accountant Before Your First Tax Season

Your second action is hiring an accountant immediately, not after your first tax season ends. A qualified Costa Rican accountant costs roughly 500 to 1,500 dollars annually depending on portfolio complexity, but they prevent penalties that start at $2,000 for shareholder declaration failures and escalate to nearly $79,000 for corporate noncompliance. They also identify whether you qualify for the old system that taxes net income instead of the flat 15% rate, potentially saving thousands in annual tax liability.

Interview accountants who specifically handle rental property taxation and ask for references from other foreign landlords. Request they explain the difference between your two filing options in writing before you hire them. A local accountant who understands your specific property costs, corporate structure, and long-term portfolio goals transforms tax compliance from guesswork into strategy.

Document Every Transaction and Expense

Your third action demands meticulous documentation of every rental transaction and deductible expense. If you operate under the standard 15% deduction system, document gross rental income through electronic invoices from your short-term rental platform or lease agreements, but do not waste time collecting expense receipts since you cannot claim individual deductions. If you qualify for the old system, electronic invoices become critical.

Hacienda cross-checks factura electrónica records automatically, and mismatched invoices trigger audits. Property management fees, repair contracts, utility payments, HOA contributions, and maintenance work must all flow through electronic invoicing. Contractors issue digital invoices, utility companies provide them automatically, and HOA administrators can supply them if requested.

Create a shared folder in cloud storage with subfolders for each expense category, and upload invoices the moment you receive them. This prevents the December panic when you realize you have lost critical documentation. Establish a monthly review habit where you reconcile your bank account against your accounting software and verify that all rental deposits and expense withdrawals match your records.

Maintain Monthly Records for Audit Readiness

When you work with an accountant, they review these monthly records during your annual filing, catching discrepancies before submission to Hacienda. This proactive approach transforms tax compliance from a stressful annual event into a manageable monthly routine. Monthly discipline protects your income and keeps your property operation on solid legal ground. Your accountant uses these organized records to identify tax-saving opportunities you would otherwise miss, whether that means switching to the old system or optimizing your expense documentation for maximum deductibility.

Final Thoughts

Rental tax compliance in Costa Rica requires three non-negotiable actions: understanding your filing obligations under the 15% standard deduction or the old system, documenting every transaction with electronic invoices, and maintaining organized records year-round. The difference between landlords who stay compliant and those who face penalties comes down to whether they treat tax management as a core business function or an afterthought. You now know that the flat 15% deduction rarely matches your actual expenses, that corporate structures unlock alternative tax calculations, and that electronic invoicing is not optional-Hacienda cross-checks these records automatically.

Staying on top of your rental tax compliance CR obligations protects your income, prevents costly audits, and positions your property operation for long-term growth. Landlords who file on time, maintain proper documentation, and work with qualified accountants keep thousands of dollars that others lose to penalties and missed deductions. The complexity of Costa Rica’s rental tax system makes professional support practical rather than optional.

Whether you manage your property independently or work with a professional team, your next step is connecting with a local accountant who understands rental taxation and setting up the accounting infrastructure this roadmap describes. We at Osa Property Management help property owners navigate these exact compliance challenges, and we recognize that most landlords benefit from expert guidance to apply the rules correctly. Contact Osa Property Management to discuss how we can support your rental income goals while keeping you compliant.