Owning rental property in Costa Rica comes with tax obligations that many landlords overlook or misunderstand. The good news is that rental tax in Costa Rica follows clear rules, and knowing them helps you keep more of your income.

At Osa Property Management, we’ve seen firsthand how proper tax planning protects your bottom line. This guide walks you through the rates, deductions, and common mistakes that cost landlords real money.

How Rental Income Tax Works in Costa Rica

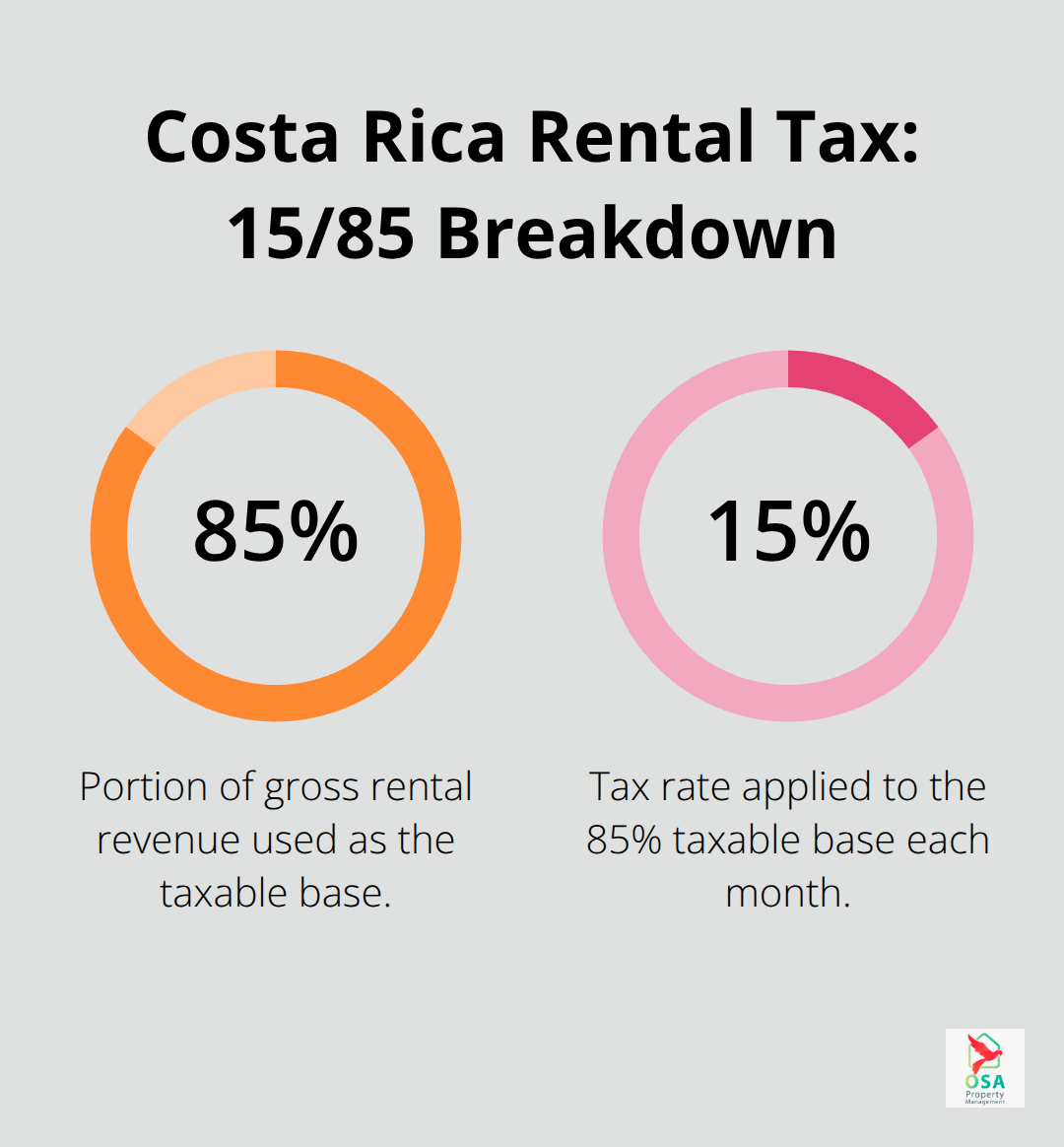

Costa Rica taxes rental income at 15% on 85% of your gross rental revenue, according to the Costa Rican tax authority Hacienda. This means you pay tax on 85% of what tenants actually pay you, without deducting most operating expenses first. If you rent a property for $2,000 per month, you owe tax on $1,700 (85% of gross), at a 15% rate, equaling $255 monthly. This 15/85 rule applies to most landlords and requires monthly filing and payment. The only alternative is if you employ staff at the rental property and elect the older net income method, which allows you to deduct expenses before calculating tax.

That approach requires annual filing instead and works best with professional guidance from a tax advisor who understands Costa Rican property law.

The 15/85 Rule Explained

Under the 15/85 rule, you cannot deduct typical operating expenses like maintenance, repairs, or property management fees from your gross income before the tax calculation happens. However, you can claim deductions on your annual tax return to reduce taxable income further. This two-step process confuses many landlords who expect to subtract costs upfront. The monthly 15% payment on 85% of gross revenue remains fixed, while your annual return captures the deductions that lower your overall tax liability.

Expenses You Can Deduct

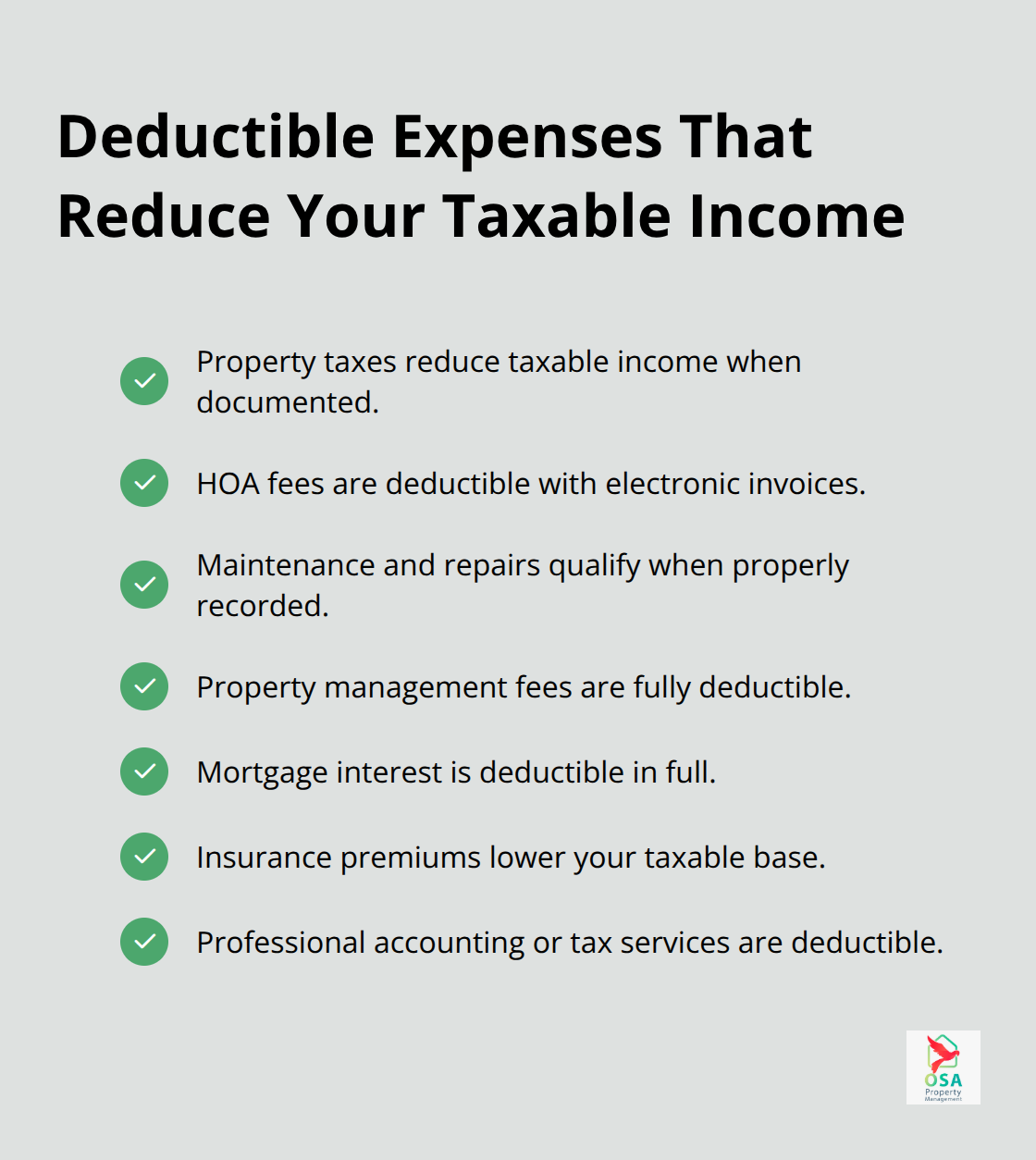

Deductible expenses include property taxes (0.25% of your property’s assessed value annually), HOA fees, maintenance and repairs, property management fees, mortgage interest, insurance premiums, and professional accounting or tax services. If your property is worth $250,000, you pay roughly $625 per year in property tax alone. These deductions stack up quickly and significantly reduce what you owe at tax time.

Documentation Requirements

Document every expense with electronic invoices through Costa Rica’s factura electrónica system because Hacienda now requires digital platforms to report host income, increasing scrutiny of vacation rental earnings. A kitchen renovation costing $10,000 includes 13% VAT, totaling $11,300, and that VAT expense helps substantiate your deductions. Track these carefully because proper documentation separates landlords who keep their money from those who face penalties for insufficient records. Without electronic invoices, Hacienda may reject your deductions entirely, leaving you to pay tax on inflated income figures.

When the Net Income Method Makes Sense

If you employ staff at your rental property (such as a caretaker or cleaner), you can elect the net income method instead of the 15/85 rule. This older system allows you to deduct all legitimate business expenses before calculating your tax liability, potentially saving thousands annually. You file taxes annually rather than monthly under this approach. A tax professional should evaluate whether this method benefits your specific situation, as the rules and thresholds vary based on your property type and staffing structure. The decision between the two methods affects your cash flow and compliance obligations significantly, so professional guidance matters here.

What Expenses Really Lower Your Rental Tax Bill

The 15/85 rule makes most landlords think they cannot deduct expenses, but that assumption costs money. While you pay monthly tax on 85% of gross income without deducting operating costs upfront, you absolutely can claim deductions on your annual tax return to reduce your overall tax liability. Property taxes, HOA fees, maintenance, repairs, management costs, mortgage interest, insurance, and professional accounting fees all count. If your property costs $250,000 and you pay $625 yearly in property tax alone, plus $1,800 annually in HOA fees, you have $2,425 in immediate deductions before you touch maintenance or management expenses. Most landlords fall into a trap: they fail to track and document these costs throughout the year, then scramble during tax season to reconstruct receipts.

Hacienda requires electronic invoices through the factura electrónica system for every expense claim, so documentation must be digital to count as a deduction. Without proper electronic records, Hacienda simply rejects your claims, leaving you taxed on inflated income.

Property Management Fees Save More Than They Cost

If you hire a property manager, that fee directly reduces your taxable income dollar-for-dollar at year-end. Long-term rental management typically runs 8–12% of monthly rent, while short-term management costs 15–25%, but both are fully deductible. A property that generates $2,000 monthly rent with a 10% management fee means $200 monthly goes to your manager, yet you recoup roughly $30 of that through reduced taxes at your 15% rate. More importantly, a professional manager ensures electronic invoicing for utilities, repairs, and HOA fees, capturing deductions you would miss alone. The real cost of management is lower than the stated percentage because the deduction itself reduces your tax burden.

Maintenance, Repairs, and Insurance Stack Quickly

Maintenance and repair expenses are fully deductible, and they accumulate fast in Costa Rica’s tropical climate. Annual maintenance reserves should run 5–8% of your property value to account for humidity damage, saltwater corrosion on coastal properties, and general wear. A $250,000 property should budget $12,500–$20,000 yearly for maintenance alone, and every receipt documented through electronic invoicing counts as a deduction. Insurance premiums for property and liability coverage are also fully deductible, typically running $400–$800 annually depending on property value and location. Mortgage interest, if you financed your purchase, is deductible in full. A $200,000 mortgage at 6% interest costs $12,000 yearly, and all of that reduces taxable income. These four categories-maintenance, insurance, mortgage interest, and management fees-often total $18,000–$35,000 annually on a mid-range property, meaning your actual tax bill drops significantly from what the 15/85 rule appears to impose.

Electronic Invoicing Separates Smart Landlords from the Rest

The factura electrónica system is not optional-it is the foundation of your tax defense. Hacienda now requires digital platforms to report host income, increasing scrutiny of vacation rental earnings and making proper documentation non-negotiable. A contractor who provides a paper receipt instead of an electronic invoice leaves you vulnerable because Hacienda will reject that expense claim. You must verify that every vendor-from plumbers to electricians to property managers-issues electronic invoices for their work. This single step determines whether you keep thousands in deductions or lose them to audit penalties. Properties managed through professional firms that handle electronic invoicing automatically capture these deductions, while landlords who manage properties themselves often miss them entirely.

What Happens When You File Your Annual Return

Your monthly 15% payment on 85% of gross revenue is not your final tax bill-it is an advance payment. When you file your annual tax return, you claim all documented deductions, and Hacienda recalculates your actual liability. If your deductions total $25,000 on $24,000 in annual gross rental income, your taxable base shrinks dramatically, and you may receive a refund of overpaid monthly taxes. This is why landlords who skip annual filing leave money on the table. The annual return is where the real tax savings happen, and it requires that you have electronic invoices for every single deductible expense. Without them, you cannot prove your claims, and Hacienda will assess you on the full 85% of gross income. The next section covers the common mistakes that prevent landlords from capturing these deductions and how to avoid them.

Where Landlords Lose Money on Taxes

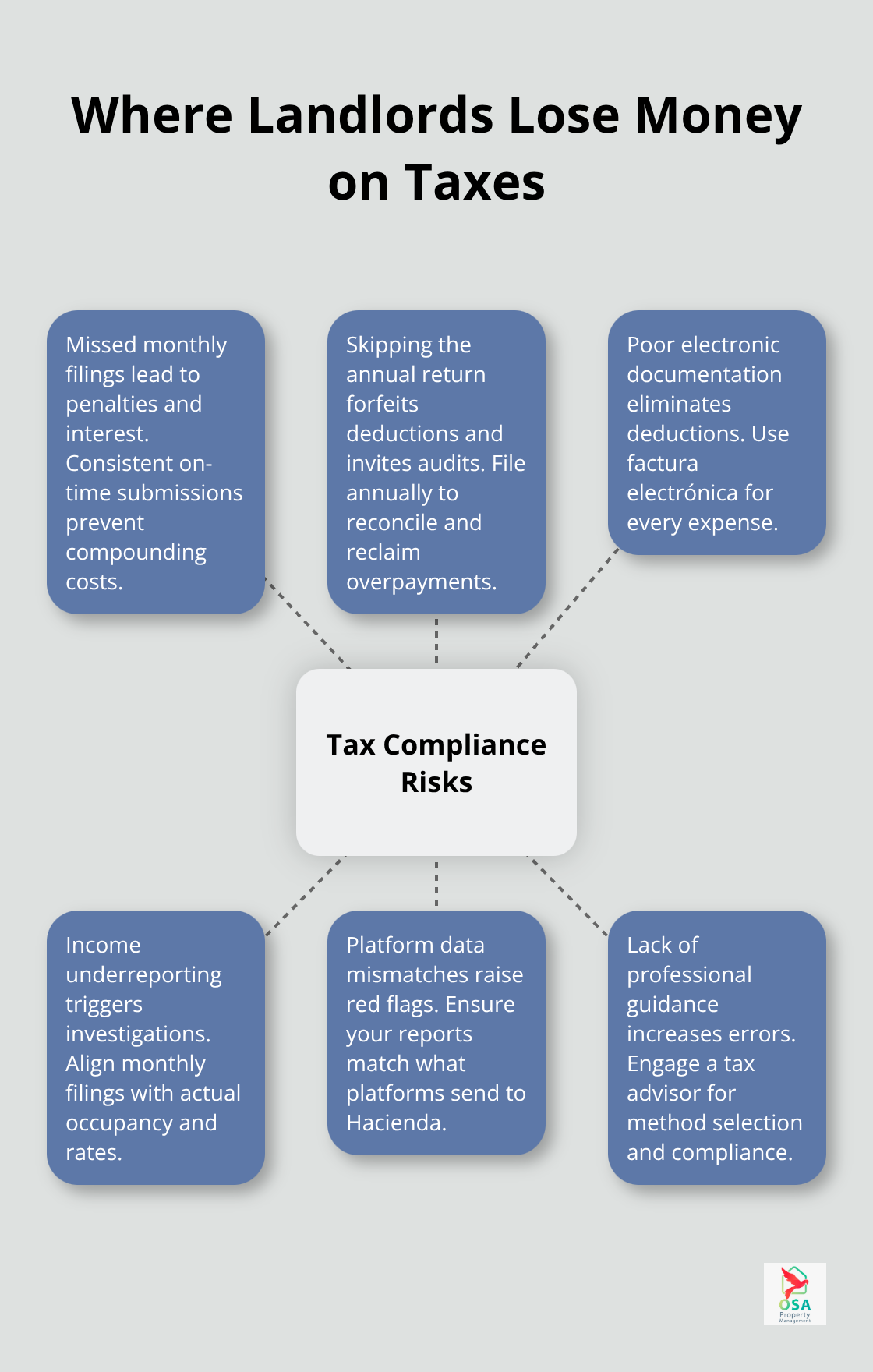

Most rental property owners in Costa Rica make one fatal mistake: they treat the monthly 15% payment on 85% of gross income as their final tax obligation and stop there. Hacienda requires monthly filings, and landlords who miss even one deadline face penalties that compound quickly. The Costa Rican tax authority imposes interest charges on late payments, and repeated non-compliance triggers audits that expose years of incomplete documentation. You must file and pay every month without exception, regardless of whether you collected rent that month.

Missing a single deadline costs far more than the five minutes required to file online.

The Annual Return Mistake That Costs Thousands

Many landlords never file an annual tax return at all, believing the monthly payments settle their obligations completely. This assumption leaves thousands of dollars in deductions unclaimed and invites audit scrutiny because Hacienda tracks who files annually and who does not. The electronic invoicing system, the factura electrónica, now feeds directly to Hacienda’s servers, meaning your rental income is already reported by digital platforms like Airbnb before you file anything. If your monthly filings and annual returns do not match what Hacienda sees from platform reports, an audit follows automatically. Landlords who skip the annual return create a paper trail mismatch that signals red flags to tax authorities.

Documentation Failures That Eliminate Deductions

The second killer mistake is failing to capture deductions through proper electronic documentation. You can claim property taxes, HOA fees, maintenance, insurance, mortgage interest, and management fees, but only if you have factura electrónica receipts proving each expense. A contractor who hands you a handwritten receipt or a simple email invoice leaves you defenseless in an audit because Hacienda rejects non-digital documentation entirely. Landlords who manage properties independently often lose thousands annually in unclaimed deductions simply because they failed to request electronic invoices from vendors. Professional property management firms ensure every utility bill, repair, and management fee generates a compliant digital receipt that substantiates deductions.

Income Reporting Gaps That Trigger Investigations

The third mistake is underreporting income by omitting months when properties sat vacant or rents were reduced. Hacienda expects your filings to match occupancy rates and rental rates documented elsewhere, so claiming zero income for a month when a platform reported bookings triggers immediate investigation. Your tax filings must align with what platforms report to Hacienda, and any gaps invite penalties depending on the severity of the discrepancy. Transparency in monthly filings protects you far more than attempting to hide income ever will. Digital platforms now report your earnings directly to tax authorities, making income concealment impossible and counterproductive.

Final Thoughts

Rental tax in Costa Rica rewards landlords who stay organized and file consistently. The 15/85 rule appears simple on the surface, but your actual tax burden depends entirely on capturing deductions through electronic invoicing and filing annual returns. Missing even one monthly deadline or skipping your annual return costs thousands in lost deductions and invites audit penalties that compound quickly.

Professional tax guidance separates successful property owners from those who overpay year after year. Costa Rica’s tax system has grown more sophisticated, with digital platforms reporting your income directly to Hacienda and the factura electrónica system tracking every transaction. Attempting to manage this alone leaves you vulnerable to rejected deductions and compliance gaps that trigger investigations.

We at Osa Property Management handle rental tax Costa Rica compliance as part of our full-service offering, managing electronic invoicing for utilities, repairs, and HOA fees so your deductions never slip through the cracks. Either commit to meticulous record-keeping and monthly filing yourself, or partner with a professional who handles it for you.