Rental property owners in Costa Rica face a complex tax landscape that catches many off guard. At Osa Property Management, we’ve seen firsthand how confusion about rental taxes Costa Rica leads to costly mistakes.

This guide walks you through what you owe, what you can deduct, and how to stay on the right side of the tax authorities.

How Rental Income Gets Taxed in Costa Rica

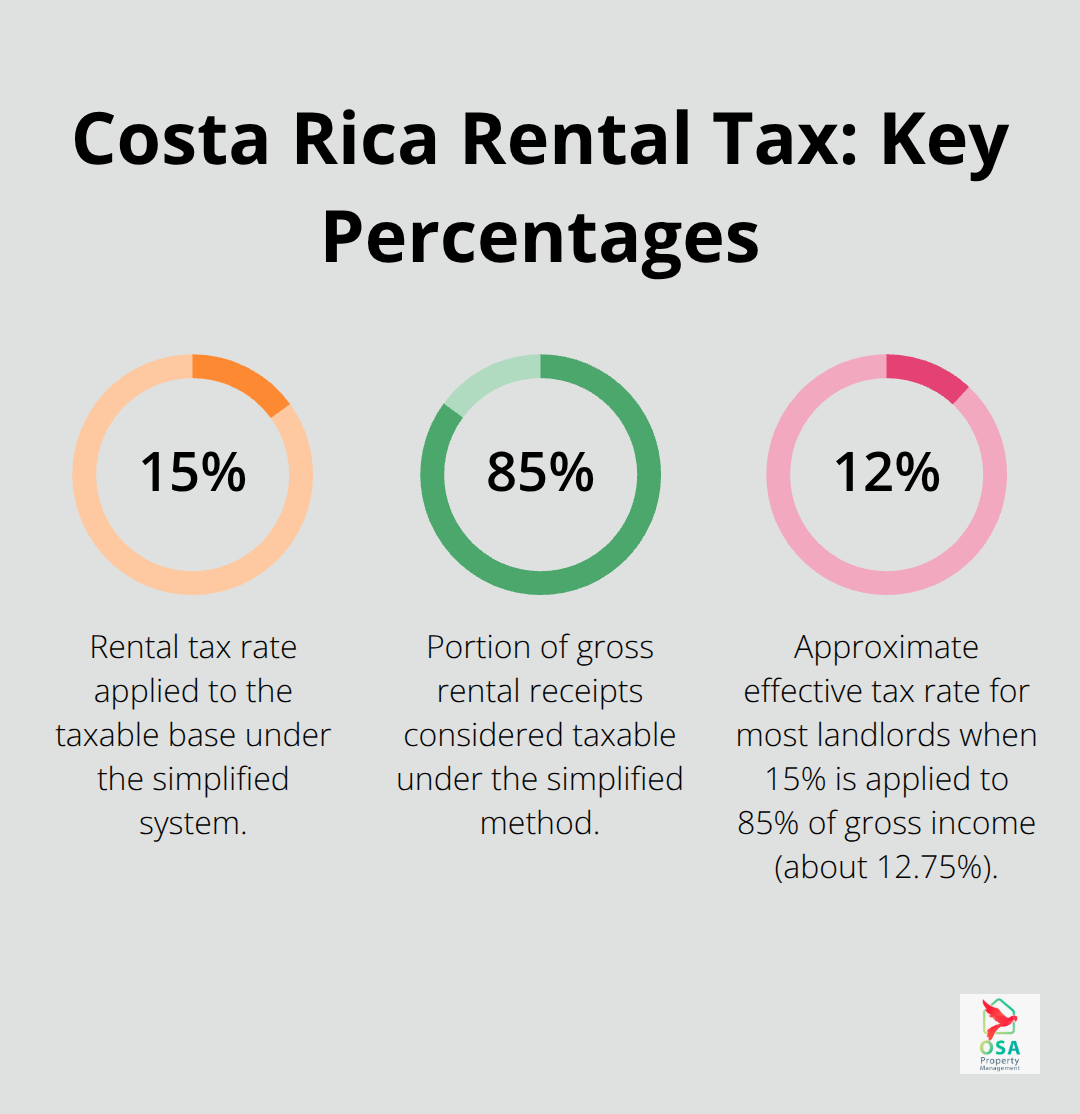

Costa Rica taxes rental income under a simplified system that most property owners find straightforward once they understand the mechanics. The tax authority applies a flat 15% rate on 85% of your gross rental receipts, which works out to an effective tax of roughly 12.75% for most landlords according to the Ministerio de Hacienda rental income guide.

The Simplified Regime vs. Traditional Regime

The simplified regime means you don’t itemize deductions-the system automatically assumes 15% of your gross income covers legitimate expenses like maintenance, insurance, and management fees. The remaining 85% gets taxed at 15%. However, this automatic deduction only works if your actual expenses stay below that 15% threshold. If your property management fees, repairs, utilities, and insurance exceed 15% of gross rental income, you can elect the traditional regime instead and deduct your real expenses. Many owners with properties in high-maintenance areas or those paying significant management fees find the traditional regime saves them money. The choice between regimes directly affects your bottom line, so calculating both scenarios before filing makes sense.

Filing Requirements for All Owners

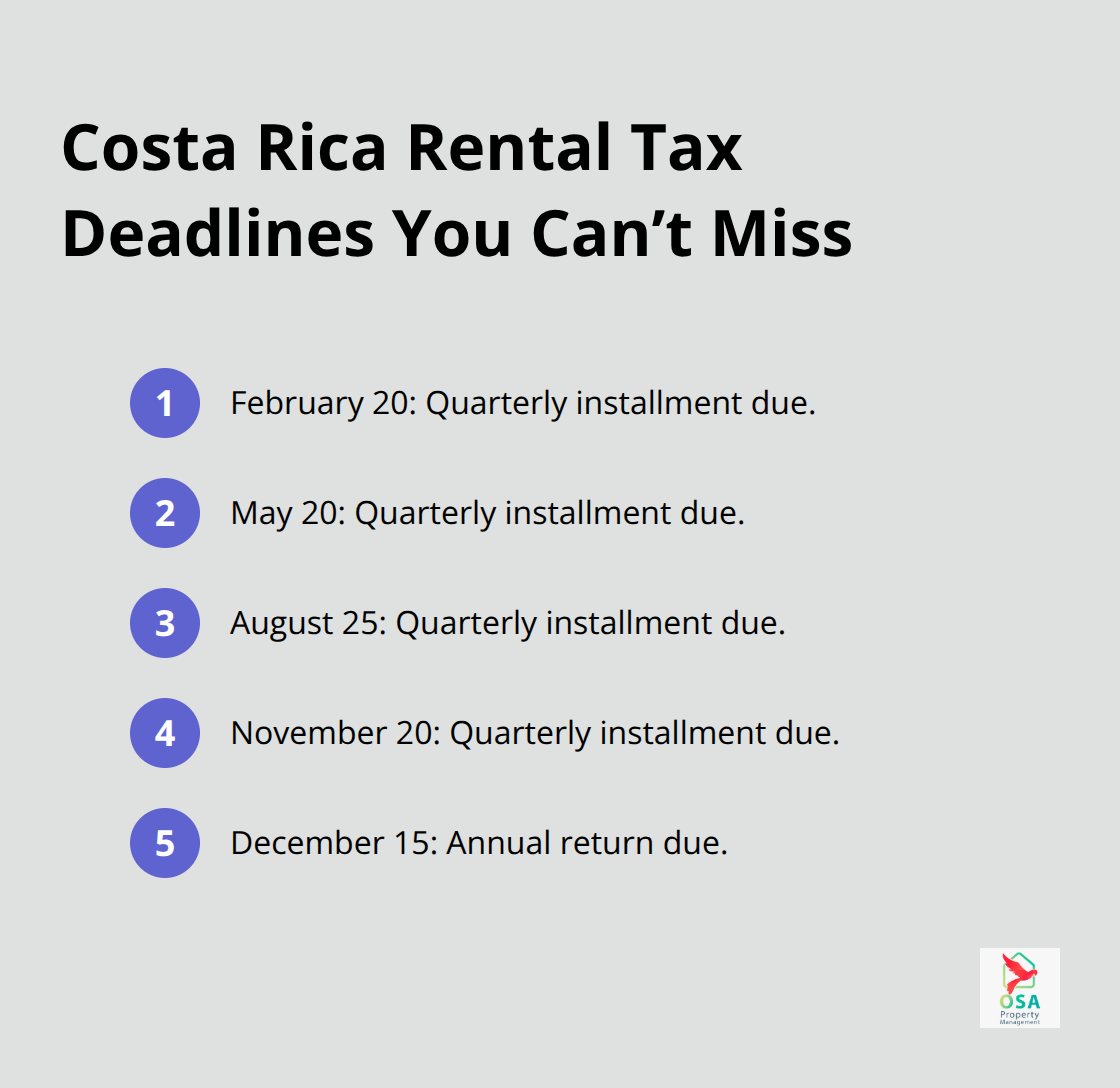

If you own rental property in Costa Rica and earn income from it, you must file regardless of residency status. Non-resident owners pay the same 15% rental tax rate as residents but must first register with Hacienda and obtain a tax ID (NIT). The Costa Rican tax year runs October 1 to September 30, not the calendar year. Your annual return is due by December 15 following the tax year end.

Quarterly Payments and Monthly Reporting

Before that deadline, you’ll make quarterly installment payments on February 20, May 20, August 25, and November 20 to avoid penalties. Monthly reporting on Form D-125 helps distribute your tax burden across the year rather than facing a large bill in December. Digital platforms like Airbnb report renter income directly to tax authorities, so your platform records must match what you file-any discrepancies invite audits.

Setting phone reminders for each quarterly deadline costs nothing and prevents costly mistakes. Many property owners set up automated payments through their Costa Rican bank account to eliminate the risk of missing dates entirely.

Understanding which regime fits your situation and staying on top of deadlines sets the foundation for tax compliance. The next section covers which expenses you can actually deduct and how to document them properly.

What Expenses Actually Lower Your Rental Tax Bill

The gap between what you think you can deduct and what the tax authority accepts costs owners thousands annually. Under the simplified regime, you receive an automatic 15% deduction regardless of your actual expenses, so claiming individual deductions makes no sense unless you switch to the traditional regime. If you make that switch, the rules become strict about documentation.

Maintenance, Repairs, and Capital Improvements

Property maintenance and repairs qualify for deductions, but only if you keep the corresponding factura electrónica from your contractor. Painting a rental unit, fixing a broken water heater, or replacing roof tiles all qualify. What does not qualify: capital improvements that increase the property’s value permanently, like adding a new room or upgrading from a basic kitchen to a high-end one. The tax authority distinguishes between keeping the property functional and making it better, and they audit this distinction aggressively.

Management Fees and Professional Services

Management fees paid to a professional company are fully deductible under the traditional regime because they represent actual money leaving your account. If you self-manage, you cannot claim a management fee for your own time. Owner-paid utilities including water, electricity, and internet are deductible if the lease requires the owner to cover them. Insurance premiums for the rental property itself are deductible, but not liability insurance for your personal assets.

Annual property tax, calculated at 0.25% of the municipal registered value, is deductible. Mortgage interest is deductible; mortgage principal payments are not.

The Factura Electrónica Requirement

The critical detail most owners miss: the factura electrónica requirement. Costa Rica’s tax authority requires digital invoices for every single deductible expense. A contractor’s handwritten receipt or a bank transfer with no invoice attached gives you zero deduction credibility during an audit. Digital accounting software like QuickBooks Online or Xero with bank feed integration catches expenses automatically and categorizes them by type, cutting the time spent on manual entry from hours to minutes monthly.

Separate Bank Accounts and Digital Records

Set up a separate business bank account for rental income and expenses immediately, before your first dollar arrives. This separation makes tax time straightforward because every transaction is already sorted by function. Many owners who skip this step face audits because their personal and rental finances are intertwined, forcing them to reconstruct years of transactions. The Ministerio de Hacienda has increased scrutiny on rental properties listed on platforms like Airbnb, cross-referencing platform reports against filed tax returns. Your accounting must match what Airbnb reported to authorities, or discrepancies trigger audits automatically.

Professional Tax Reviews and Compliance Support

Quarterly tax reviews with a local professional cost roughly $100 to $300 per review but catch mistakes before penalties apply. Professional property management services handle accounting and tax compliance for their clients, which eliminates the guesswork entirely and ensures deductions align with what authorities expect in your region. The mistakes you make with deductions pale in comparison to the errors that occur when you fail to report income in the first place-a problem we address in the next section.

Common Mistakes Rental Property Owners Make

The most expensive mistake rental property owners make in Costa Rica isn’t claiming a questionable deduction-it’s failing to report income in the first place. Digital platforms like Airbnb report your rental receipts directly to the Ministerio de Hacienda, creating a permanent record that tax authorities cross-reference against filed returns. If you earned $50,000 in platform-reported income but filed taxes on $40,000, the discrepancy triggers an automatic audit. The penalties for underreporting rental income start at 25% of the unpaid tax and climb to 100% if authorities determine the omission was intentional. Many owners rationalize that unreported cash payments won’t appear anywhere, but this logic ignores the reality that Airbnb, Booking.com, and VRBO all file reports with Costa Rican tax authorities monthly. The solution is straightforward: report every dollar of rental income, whether it arrives through a platform, direct bank transfer, or physical cash. Your Form D-125 monthly filing and annual return must match what platforms reported, down to the dollar.

Undocumented Deductions Trigger Audits

Claiming deductible expenses without a single factura electrónica guarantees that an audit will disallow every penny and add penalties on top. The tax authority doesn’t care about your memory of what you spent or your good intentions-they want digital proof. A contractor’s verbal estimate, a handwritten receipt, or a bank statement showing a transfer to a repair company means nothing without the corresponding official invoice. If you paid a plumber $500 to fix a leak but have no invoice, that $500 disappears from your deduction entirely during an audit. The factura electrónica requirement applies to every expense category: management fees, utilities, insurance, property taxes, and repairs. Owners often claim depreciation without understanding that depreciation recapture on sale creates unexpected tax liability when they eventually sell, turning what seemed like a deduction into a future tax bill. The traditional regime requires meticulous record-keeping; the simplified regime sidesteps this problem entirely by applying an automatic 15% deduction that requires no documentation at all. If your actual expenses fall below 15% of gross rental income, the simplified regime always delivers the better outcome because you receive the deduction without maintaining thousands of invoices.

Missed Quarterly Deadlines Cost Penalties and Interest

Missing a quarterly tax installment payment deadline costs you penalties and interest that accumulate faster than most owners realize. The February 20, May 20, August 25, and November 20 deadlines are firm-there is no grace period, no extension, and no forgiveness. A payment submitted on February 21 is late, triggering penalties that compound monthly. The Ministerio de Hacienda charges interest on late payments at rates that exceed 10% annually, meaning a missed $3,000 payment in February costs an extra $300 by year-end in interest alone before penalties apply. Many owners who self-manage rental properties forget these dates entirely because they focus on guest communications, maintenance issues, and booking management. Setting up automatic payments through your Costa Rican bank account eliminates this risk completely-the payment processes on the exact date, every time, without requiring you to remember or manually initiate anything. Professional property management handles this automatically as part of their service, ensuring no deadlines slip through the cracks. The annual return due December 15 is equally absolute; filing one day late invites penalties that start at 5% of the tax owed and increase monthly.

Final Thoughts

Rental taxes in Costa Rica demand attention to three core obligations: you must report all income accurately, document every deductible expense with a factura electrónica, and hit quarterly payment deadlines without exception. The simplified regime eliminates documentation headaches by applying an automatic 15% deduction, making it the right choice for most owners whose actual expenses fall below that threshold. The traditional regime rewards owners with substantial documented expenses, but only if you maintain meticulous records and understand that depreciation recapture creates future tax liability on sale.

A local tax professional reviewing your situation quarterly catches mistakes before penalties apply and helps you choose the regime that actually saves money for your specific property. We at Osa Property Management handle accounting, tax compliance, and quarterly filings for our clients across the southern Pacific zone, eliminating the guesswork entirely and ensuring your deductions align with what tax authorities expect in your region. Our team manages properties in Tarcoles, Jaco, Dominical, Manuel Antonio, Ojochal, Uvita, and Golfito, and we understand the regional nuances that affect compliance.

Open a separate business bank account for rental income and expenses immediately, set up automated quarterly payments, and connect with a local professional who understands both Costa Rican and your home country tax obligations. If you own property through an entity or earn significant rental income, cross-border tax planning with qualified advisors prevents costly mistakes that compound over years. Professional property management services handle this complexity for you, freeing your time and protecting your investment from preventable penalties.