Renting out property in Costa Rica comes with tax obligations that many landlords overlook or misunderstand. Getting CR rental tax basics right from the start saves you money, headaches, and potential penalties down the road.

At Osa Property Management, we’ve seen firsthand how proper tax planning protects your rental income and keeps you compliant with local authorities. This guide walks you through everything you need to know.

Who Pays Rental Taxes in Costa Rica and What Income Counts

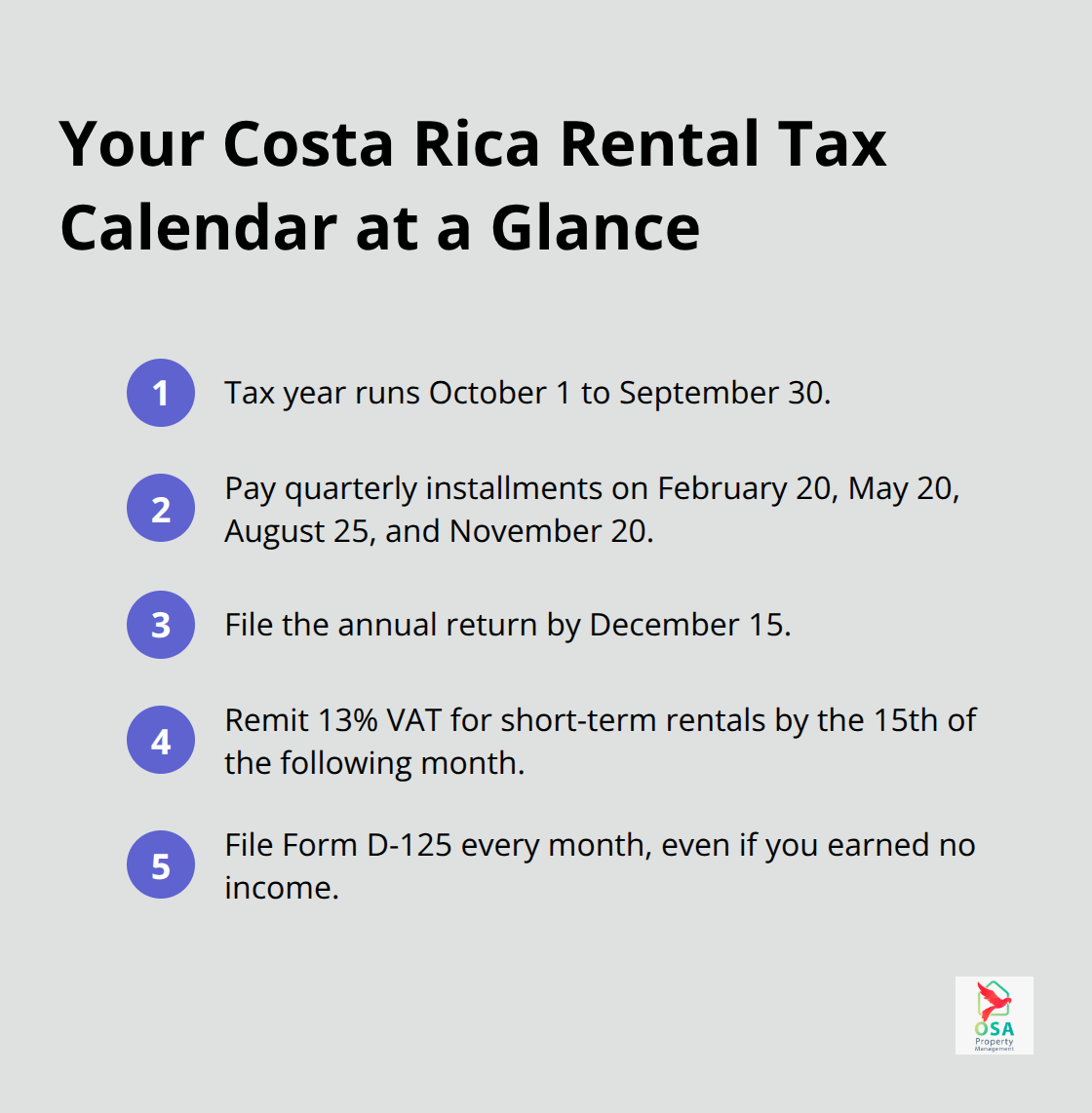

Every landlord renting property in Costa Rica-whether you own one villa or multiple units-must register with Hacienda and file taxes on rental income. Non-residents face identical tax obligations as residents; your citizenship or residency status does not exempt you. The Ministerio de Hacienda requires you to obtain a tax ID (NIT) and activate the correct economic activity code for short-term or long-term rentals. If you hold property through a corporation, corporate income tax applies on top of individual rental taxes, which is why many foreign owners structure holdings as LLCs or corporations to manage liability and deductions-but this adds complexity and requires strict compliance. Short-term rentals (stays under 30 days) trigger both income tax and a 13% VAT that you must collect from guests and remit monthly to Hacienda; long-term leases avoid VAT but still require income tax filing. Digital platforms like Airbnb report your transaction data directly to Hacienda as of 2025, so underreporting income now carries significant audit risk. The tax year runs October 1 to September 30, with quarterly installments due February 20, May 20, August 25, and November 20; the annual return is due by December 15. Monthly Form D-125 filings are mandatory regardless of whether you earned income that month.

How Much Tax You Actually Owe

Costa Rica taxes rental income under two regimes, and choosing the right one saves thousands annually. The simplified regime taxes 15% of 85% of your gross rental receipts, creating an effective rate around 12.75% according to the Ministerio de Hacienda; this regime automatically deducts 15% of gross income for maintenance, insurance, and management without requiring itemized documentation. The traditional regime allows deducting actual expenses-management fees, repairs, utilities if you pay them, property tax at 0.25% of assessed value, mortgage interest, and insurance-but demands strict electronic invoicing (factura electrónica) and offers no deductions without digital receipts. Switch to the traditional regime only if your documented expenses exceed 15% of gross income; most landlords stay with the simplified regime because it requires less paperwork. As of 2025, the first 3.8 million colones (approximately $7,600 USD) of annual rental income is tax-exempt; income above that threshold faces progressive rates from 10% to 25% depending on total earnings. Short-term rental VAT is a separate 13% liability collected from guests, not deductible from income tax, and must be remitted by the 15th of the following month. Late payments incur penalties exceeding 10% annually, so automated bank payments from a Costa Rican account eliminate missed deadlines.

The number 0% seems to be not appropriate for this chart. Please use a different chart type. Reconcile platform payouts monthly with your tax filings; Hacienda cross-references Airbnb data against your Form D-125 submissions, and mismatches trigger audits.

Why Platform Reporting Changes Everything

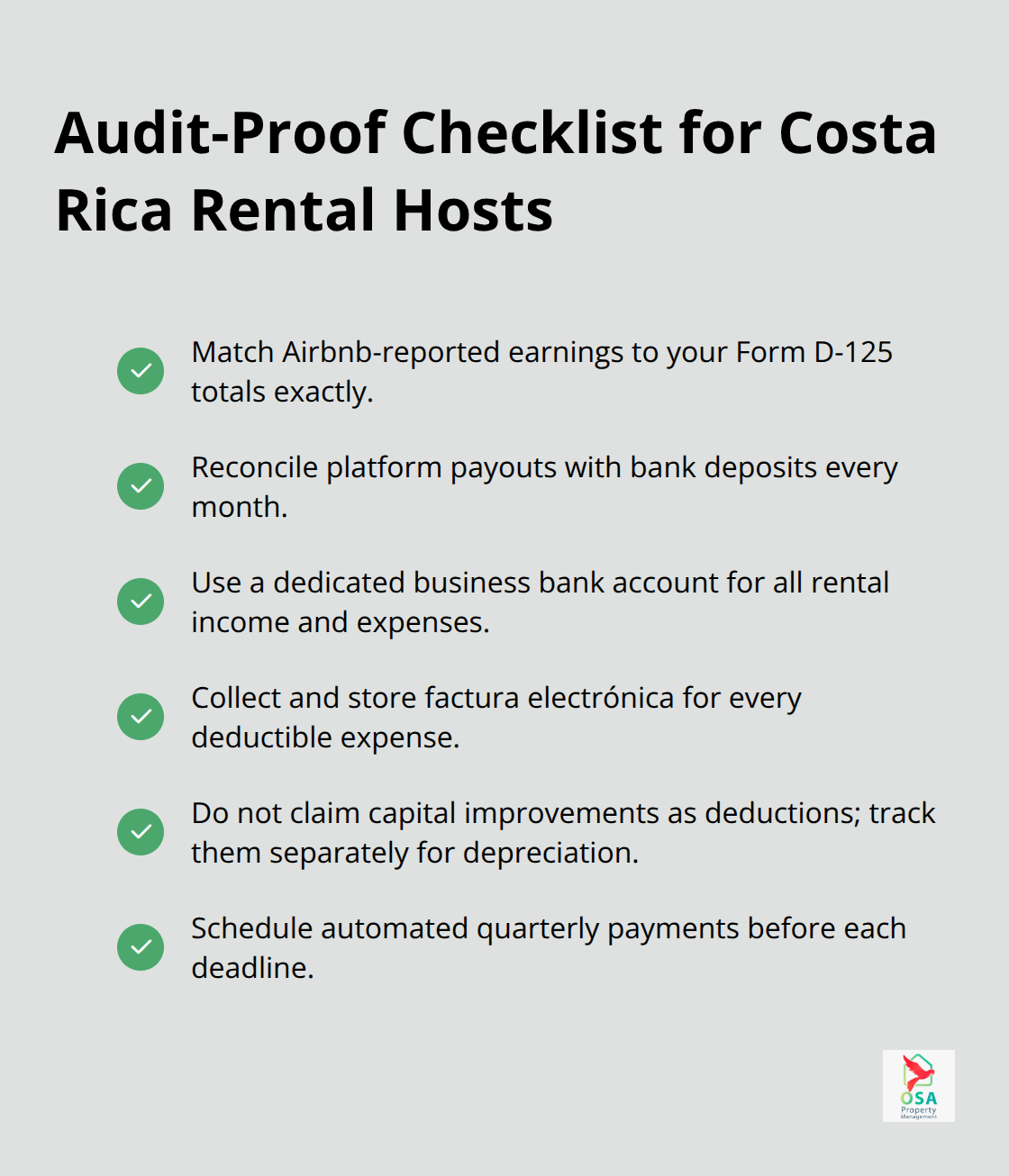

Airbnb and other digital platforms now report host earnings directly to Hacienda, fundamentally shifting how tax authorities verify your income. This transparency means you cannot underreport without detection; your platform statements and your tax filings must align exactly. Set up a single bank account for all rental deposits and expenses, then reconcile it monthly against your platform payouts and tax submissions. This practice takes 30 minutes monthly but prevents costly audit disputes later.

What Expenses Actually Count as Tax Deductions

The Gap Between What You Think You Can Deduct and What Hacienda Allows

The difference between what you think you can deduct and what Hacienda actually allows costs landlords thousands in missed deductions and audit penalties. Under the simplified regime, you lose the ability to itemize at all-the system assumes 15% of your gross income covers all expenses, period. If your actual costs run lower, you pay more tax than necessary; if they exceed 15%, you still cannot claim them under this regime. The traditional regime demands strict electronic invoicing (factura electrónica) for every single deductible expense, meaning handwritten receipts, cash payments, and bank transfers without attached invoices yield zero deduction during an audit.

Which Expenses Hacienda Actually Allows

Property management fees rank among the most valuable deductions because they directly reduce taxable income when documented with proper invoices. Maintenance and repairs-fixing a broken water heater, patching roof leaks, replacing damaged flooring-are fully deductible under the traditional regime if you retain the factura electrónica from the contractor. However, capital improvements that permanently increase property value, such as adding a new bedroom or installing a high-end kitchen renovation, cannot be deducted; these get depreciated over years, which creates future tax liability when you sell. Property tax at 0.25% of assessed municipal value is deductible annually, as is mortgage interest (though principal repayment is not). Insurance premiums for rental liability and property coverage count as deductions; personal asset liability insurance does not. Utilities you pay on behalf of tenants are deductible only if the lease explicitly requires you to cover them-if tenants pay their own electricity and water, you cannot claim those expenses.

How Most Landlords Lose Thousands in Valid Deductions

Most landlords fail to claim deductions they qualify for because they lack proper invoicing. Open a separate business bank account immediately and funnel all rental income and expenses through it. Use accounting software like QuickBooks Online or Xero with automatic bank feeds to categorize expenses in real time, eliminating the scramble to reconstruct records during tax season. When a contractor sends you an invoice, request the digital version (factura electrónica) and upload it to your accounting software on the same day-this 60-second habit prevents audit disasters. If you use a property manager, demand itemized monthly statements showing management fees, maintenance costs, utilities, and any other expenses with attached digital receipts. Reconcile these statements against your bank account each month to catch discrepancies immediately rather than discovering them during a Hacienda review.

Short-Term Rental VAT and the Regime Trap

Short-term rental VAT at 13% collected from guests is remitted separately and never deductible from income tax, so do not confuse it with deductible expenses. Many landlords switch to the traditional regime thinking they will save money, only to discover their actual documented expenses fall short of 15%-stick with the simplified regime unless your records prove otherwise. The traditional regime works only when your documented expenses genuinely exceed 15% of gross income; switching without verified numbers costs more in complexity than it saves in taxes.

Where Landlords Lose Money and Get Audited

Income Underreporting and Platform Transparency

The gap between what landlords think they’re doing right and what Hacienda actually requires grows wider every year, especially as platform reporting tightens. Underreporting income remains the costliest mistake, and it’s becoming impossible to hide. When you list on Airbnb, the platform reports your exact earnings to Hacienda monthly as of 2025, so your Form D-125 submissions must match those figures down to the colón. Hacienda cross-references platform data against filed returns automatically, and mismatches trigger audits that cost far more than the original unpaid tax. Penalties for underreporting range from 25% to 100% of the unpaid amount, plus interest exceeding 10% annually according to the Ministerio de Hacienda.

One landlord in Jacó reported 3 million colones in income on their tax filing while Airbnb showed 5.2 million colones in the same period; the difference triggered a full audit that cost thousands in professional fees and penalties that could have been avoided with accurate monthly reconciliation. The fix is straightforward: reconcile your platform payouts against your bank deposits monthly, then file your Form D-125 using those verified numbers. Spend 30 minutes on the first day of each month downloading your platform statement, comparing it to your bank account, and confirming the totals match your tax submission. This habit eliminates audit risk entirely.

Expense Deductions and Documentation Failures

Expense deductions represent the second major trap, where landlords either claim things that don’t qualify or fail to claim things that do. The traditional regime demands factura electrónica for every expense, yet most landlords keep handwritten invoices, email receipts, or bank statements without attached digital invoices-all worthless during an audit. Landlords can lose thousands in deductions simply because they can’t provide adequate documentation during an audit; one property owner in Manuel Antonio claimed $8,000 in maintenance repairs but lost the entire deduction because the contractor provided only a handwritten receipt instead of an electronic invoice, costing roughly $1,000 in additional taxes plus audit fees.

Open a dedicated business bank account today and use QuickBooks Online or Xero to automatically categorize every transaction with attached digital receipts. When a contractor or utility company sends an invoice, request the factura electrónica version immediately and upload it to your accounting software the same day. Capital improvements-new bedrooms, kitchen renovations, structural upgrades-cannot be deducted despite landlords regularly trying to claim them; these assets depreciate over years and create tax liability when you eventually sell, so keep them separate from maintenance expenses in your records.

Missed Deadlines and Preventable Penalties

Missing the quarterly installment deadlines (February 20, May 20, August 25, and November 20) triggers automatic penalties; set automated bank transfers from your Costa Rican account on the 15th of each deadline month so you never miss a payment. Late fees exceed 10% annually, and the Ministerio de Hacienda enforces these strictly, so automated payments eliminate this entirely preventable expense.

Final Thoughts

Costa Rica rental tax basics require three non-negotiable practices: report all income accurately, document every deductible expense with digital invoices, and never miss a deadline. Landlords who stay compliant and maximize deductions treat their rental property like a business, not a side income-they open a separate bank account, use accounting software, and reconcile platform payouts monthly against tax filings. The cost of ignoring these steps far exceeds the time investment required to get them right.

Hacienda’s increased scrutiny on digital platform rentals means your Airbnb or booking.com statements now serve as your tax authority’s primary verification tool. Underreporting by even 100,000 colones triggers audits that consume weeks of your time and thousands in professional fees. Conversely, landlords who file accurate Form D-125 submissions matching their platform data face zero audit risk and protect their rental income fully.

Start today by opening a dedicated business bank account, then set up QuickBooks Online or Xero to track expenses automatically. Request digital invoices from every contractor and service provider, uploading them immediately to your accounting system. We at Osa Property Management handle tax compliance, accounting, and bill payment for landlords across Jacó, Manuel Antonio, Uvita, and the southern Pacific zone, removing the administrative burden entirely so you focus on growing your rental income.